If you filed your 2025 taxes last year and felt reasonably good about the number at the bottom of your return, I have some important news: the 2026 tax brackets for retirees have changed significantly, and that same income could push you into a higher bracket this year. Not because you earned more — but because the rules changed.

The Tax Cuts and Jobs Act of 2017, the sweeping tax overhaul that lowered rates and nearly doubled the standard deduction, officially expired at the end of 2025. That means every tax return filed for 2026 income and beyond now falls under a different set of brackets, deductions, and thresholds. For retirees drawing income from multiple sources — Social Security, retirement accounts, pensions, and investments — the ripple effects could be significant.

In this article, I will walk you through exactly what changed, how it specifically affects people in or near retirement, and the concrete moves you may want to consider before the end of this year.

Table of Contents

- What Happened to the Tax Brackets

- The 2025 vs. 2026 Bracket Comparison

- Standard Deduction Changes

- How This Specifically Affects Retirees

- The Roth Conversion Window May Have Shifted — Not Closed

- IRMAA and Medicare Premium Ripple Effects

- Five Moves Retirees May Want to Consider Before Year-End

- Key Takeaways

- Frequently Asked Questions

What Happened to the Tax Brackets

The TCJA was always designed with an expiration date. When Congress passed it in late 2017, the individual tax provisions — the lower rates, the larger standard deduction, and expanded brackets — were scheduled to sunset after December 31, 2025. Despite years of speculation about whether Congress would extend, modify, or make these provisions permanent, the individual rate cuts expired as originally written.

What this means in practical terms: the federal income tax rate structure has reverted to its pre-TCJA framework, adjusted for inflation. We have gone from seven brackets with a top rate of 37% back to seven brackets with a top rate of 39.6%. But the changes are not just at the top — nearly every bracket shifted.

The 12% bracket that many retirees relied on for tax-efficient withdrawals is now 15%. The 22% bracket is now 25%. And the 24% bracket, which was a sweet spot for Roth conversion strategies, has jumped to 28%.

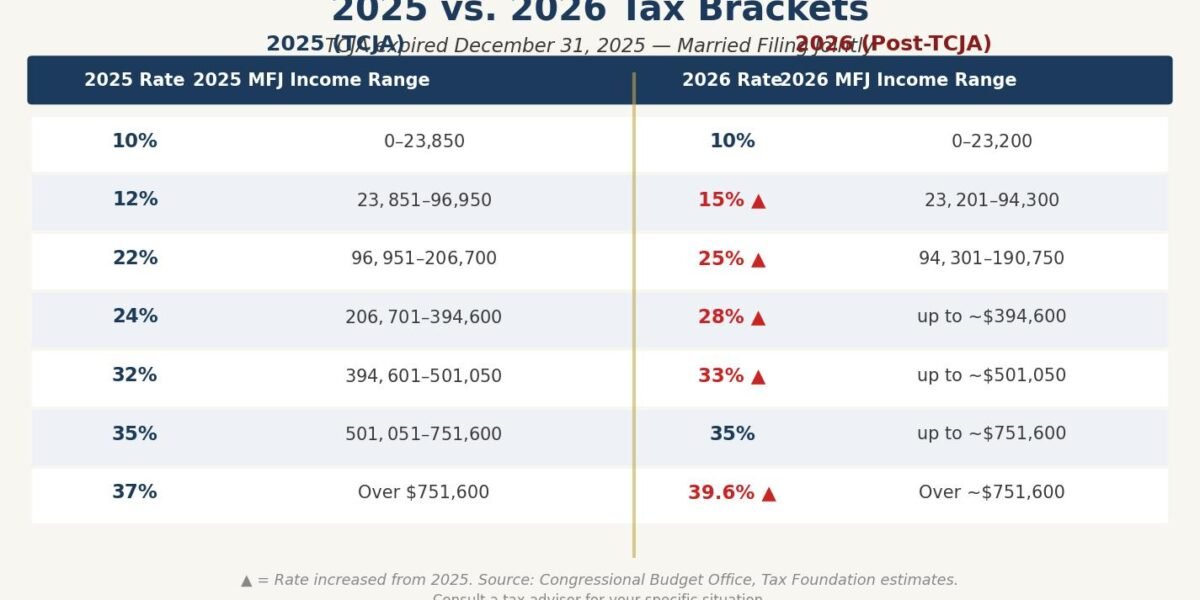

The 2025 vs. 2026 Bracket Comparison

Here is a side-by-side look at how the brackets have changed for both single filers and married couples filing jointly. These figures reflect inflation-adjusted estimates published by the Congressional Budget Office and the Tax Foundation.

Single Filers

| Tax Rate (2025) | Income Range (2025) | Tax Rate (2026) | Income Range (2026 Est.) |

|---|---|---|---|

| 10% | $0 – $11,925 | 10% | $0 – $11,600 |

| 12% | $11,926 – $48,475 | 15% | $11,601 – $47,150 |

| 22% | $48,476 – $103,350 | 25% | $47,151 – $114,300 |

| 24% | $103,351 – $197,300 | 28% | $114,301 – $237,950 |

| 32% | $197,301 – $250,525 | 33% | $237,951 – $424,950 |

| 35% | $250,526 – $626,350 | 35% | $424,951 – $480,050 |

| 37% | Over $626,350 | 39.6% | Over $480,050 |

Married Filing Jointly

| Tax Rate (2025) | Income Range (2025) | Tax Rate (2026) | Income Range (2026 Est.) |

|---|---|---|---|

| 10% | $0 – $23,850 | 10% | $0 – $23,200 |

| 12% | $23,851 – $96,950 | 15% | $23,201 – $94,300 |

| 22% | $96,951 – $206,700 | 25% | $94,301 – $190,750 |

| 24% | $206,701 – $394,600 | 28% | $190,751 – $364,200 |

| 32% | $394,601 – $501,050 | 33% | $364,201 – $462,500 |

| 35% | $501,051 – $751,600 | 35% | $462,501 – $693,750 |

| 37% | Over $751,600 | 39.6% | Over $693,750 |

Note: 2026 figures are inflation-adjusted estimates based on CBO projections. Final IRS figures for 2026 may vary slightly. Source: IRS.gov and Tax Foundation analysis.

The key takeaway from these tables is not just the rate increases — it is the bracket compression. The income ranges where lower rates apply have narrowed, meaning more of your income could be taxed at higher rates than it was last year.

Standard Deduction Changes

The TCJA’s near-doubling of the standard deduction was one of its most impactful provisions for retirees who do not itemize. Here is how the standard deduction has changed:

| Filing Status | 2025 (TCJA) | 2026 (Post-Sunset Est.) |

|---|---|---|

| Single | $15,000 | $8,300 |

| Married Filing Jointly | $30,000 | $16,600 |

| Additional (Age 65+) | $1,950 (single) / $1,550 (married, each) | Similar additional amounts |

There is a silver lining here: with the TCJA expiration, personal exemptions have returned, estimated at approximately $5,300 per person. For a married couple, that adds roughly $10,600 back in deductions. However, for most retirees filing jointly, the combined standard deduction plus personal exemptions (approximately $27,200) still falls short of the $30,000 standard deduction they had in 2025.

The net effect for a married couple over 65: you could see roughly $4,000 to $5,000 less in total deductions compared to last year, depending on your specific situation. That means more taxable income before you even look at the higher rates.

How This Specifically Affects Retirees

These changes do not exist in a vacuum. For retirees, they interact with several income streams and thresholds in ways that can compound:

Required Minimum Distributions (RMDs)

If you are 73 or older and taking RMDs from traditional IRAs or 401(k)s, your distribution is taxed as ordinary income. With the 12% bracket now at 15% and the 22% bracket at 25%, a retiree taking a $50,000 RMD on top of Social Security could see their effective tax rate climb meaningfully. The tax on that same RMD just got more expensive — without the distribution amount changing at all.

Social Security Taxation

Up to 85% of your Social Security benefits can be subject to federal income tax, depending on your combined income. The thresholds that determine how much of your Social Security is taxable ($25,000 for single filers, $32,000 for married filing jointly) have never been indexed for inflation since they were established in 1983 and 1993. With higher marginal rates now applying to the same income levels, more retirees may find a larger portion of their benefits effectively taxed at steeper rates.

For a deeper look at how Social Security taxation works, see my guide on Social Security myths that could be costing you.

Capital Gains and Investment Income

While long-term capital gains rates themselves did not change with the TCJA sunset, your ordinary income level determines which capital gains bracket you fall into. Higher ordinary income from the bracket shifts could potentially push some retirees from the 0% long-term capital gains rate into the 15% rate — a meaningful difference for those who were carefully managing taxable investment sales.

Thomas’s Take: The compounding effect is what catches people off guard. It is not just that one bracket went up — it is that higher marginal rates, a smaller standard deduction, and unchanged Social Security thresholds all push in the same direction. A retiree with $80,000 in total income could easily see their federal tax bill increase by $2,000 to $4,000 compared to last year.

The Roth Conversion Window May Have Shifted — Not Closed

One of the most popular strategies in recent years has been executing Roth conversions while the TCJA rates were low. That window at the 12% and 22% brackets was historically attractive.

Now that those brackets are 15% and 25%, does the Roth conversion strategy still make sense? For many retirees, the answer is still yes — but the math has changed.

Here is why Roth conversions may still be worth considering:

Free Download: Social Security Optimization Guide

Learn the strategies that could maximize your lifetime Social Security benefits.

Get Your Free Copy- Tax rates could go higher in the future. The current post-sunset rates are not necessarily the ceiling. Future legislation, growing deficits, or policy changes could push rates higher still.

- RMDs create forced taxable income. Converting some traditional IRA assets to Roth now — even at 25% — could reduce future RMDs that might otherwise be taxed at 28% or 33% as your balance grows.

- Roth accounts have no RMDs. This gives you more control over your taxable income in later years and can benefit heirs who inherit the account.

The key is running the numbers for your specific situation. A conversion that fills up the 15% bracket (roughly $94,300 of taxable income for a married couple) could still be a smart long-term play if the alternative is paying 25% or higher on those same dollars later.

IRMAA and Medicare Premium Ripple Effects

If you are on Medicare, the tax bracket changes have a secondary consequence that many people overlook: Income-Related Monthly Adjustment Amounts (IRMAA).

IRMAA surcharges on Medicare Part B and Part D premiums are based on your modified adjusted gross income (MAGI) from two years prior. The 2026 IRMAA brackets use your 2024 income — so the TCJA was still in effect for that determination. However, decisions you make in 2026 under the new rates will affect your 2028 IRMAA.

Higher marginal rates may push some retirees to adjust their income strategies. For instance, a large Roth conversion or capital gains realization in 2026 that pushes your MAGI above $218,000 (married filing jointly) could trigger IRMAA surcharges of several hundred dollars per month in 2028 — for both you and your spouse.

For more on how Medicare costs interact with retirement income, see my article on 2026 Medicare changes every pre-retiree should know.

Pro Tip: When evaluating any income-generating strategy in 2026, always run an IRMAA projection alongside the tax calculation. The surcharge can add $1,000 to $5,000+ annually in Medicare premiums, and it applies per person — so a married couple could face double the impact.

Five Moves Retirees May Want to Consider Before Year-End

While everyone’s situation is different, here are five strategies that many retirees and pre-retirees may want to explore with their financial advisor before December 31:

1. Revisit Your Withdrawal Sequencing

The order in which you draw from taxable, tax-deferred, and tax-free accounts matters more than ever. With higher rates, pulling from Roth accounts in years when your taxable income is elevated could help keep you in a lower bracket. Review my guide on withdrawal mistakes that cost retirees thousands for more detail.

2. Run a Roth Conversion Analysis for the New Brackets

Even though the 12% bracket is gone, converting up to the top of the 15% or 25% bracket could still be advantageous depending on your projected future tax rates and RMD trajectory. The key is comparing the tax you would pay now versus the tax you would likely pay later.

3. Evaluate Charitable Giving Strategies

With the lower standard deduction, more retirees may benefit from itemizing again — especially if they bunch charitable contributions. Qualified Charitable Distributions (QCDs) from IRAs remain one of the most tax-efficient giving strategies for those 70½ and older, since the distribution satisfies your RMD without adding to your taxable income.

4. Check Your Estimated Tax Payments

If you have been making quarterly estimated payments based on 2025 rates, your 2026 liability could be higher. Underpayment penalties are avoidable if you adjust your estimates now rather than facing a surprise in April 2027.

5. Consider Tax-Loss Harvesting Opportunities

With higher ordinary income tax rates, the value of offsetting gains with losses has increased. If you hold investments with unrealized losses, strategically harvesting those losses could reduce your taxable income and potentially keep you below key thresholds like IRMAA brackets.

Key Takeaways

- The TCJA’s individual tax provisions expired at the end of 2025, returning tax brackets to higher rates — the 12% bracket is now 15%, 22% is now 25%, and the top rate is back to 39.6%.

- The standard deduction has been roughly cut in half, though the return of personal exemptions partially offsets this. Most retirees will still see a net increase in taxable income.

- Retirees face compounding effects from higher bracket rates, smaller deductions, unchanged Social Security taxation thresholds, and potential IRMAA surcharge triggers.

- Roth conversions remain relevant but require updated analysis under the new rate structure — converting at 15% or 25% may still beat paying 28% or higher on future RMDs.

- Year-end planning is more important than ever. Withdrawal sequencing, estimated tax adjustments, charitable strategies, and tax-loss harvesting all deserve a fresh look under the 2026 rules.

Frequently Asked Questions

Did all the TCJA tax provisions expire in 2026?

The individual income tax rate reductions, the expanded standard deduction, and several other provisions affecting individual filers expired at the end of 2025. Some corporate provisions, including the reduced 21% corporate tax rate, were made permanent and remain in effect. The provisions affecting individual retirees — brackets, deductions, and personal exemptions — are the ones that changed.

How much more could I owe in taxes for 2026?

The impact varies significantly based on your income sources and filing status. As a rough illustration, a married couple with $80,000 in combined taxable income from Social Security, RMDs, and pensions could see their federal tax increase by approximately $2,000 to $4,000 compared to 2025. A couple with $150,000 in taxable income could see an even larger jump. These are hypothetical estimates — your actual impact depends on your specific situation.

Should I still do Roth conversions now that rates are higher?

For many retirees, Roth conversions remain a potentially valuable strategy even at the higher rates. The question is not whether 15% or 25% is low in absolute terms, but whether it is lower than the rate you would pay on those dollars in the future. If your traditional IRA balance is growing and your future RMDs could push you into the 28% or 33% bracket, converting some of that balance now could still result in long-term tax savings. Running a personalized projection with a financial advisor is the best way to evaluate this.

These tax changes affect virtually every retiree’s financial picture, but the good news is that there are concrete steps you can take to manage the impact. The worst approach is to do nothing and hope it works out — the best approach is to understand the new landscape and make informed adjustments.

If you have questions about how the 2026 tax bracket changes affect your specific retirement plan, I am always here to help.

Thomas Clark is a Senior Lead Wealth Advisor at Confluence Capital Management, LLC. Investment advisory services offered through Altitude Capital Management, LLC, an SEC-registered investment advisor. Content on this site is for educational and informational purposes only and does not constitute personalized investment advice. Past performance is not indicative of future results. Consult with a qualified financial professional before making any investment decisions.

Thomas Clark is a Series 65 licensed investment advisor and experienced trader. He specializes in investing, retirement planning, and market analysis, helping individuals build wealth and make informed financial decisions.