The Bucket Planning Approach to Retirement Income

You have spent 30 or 40 years building a nest egg. Now comes the question nobody fully prepares you for: how do you actually turn that lump sum into a reliable paycheck that lasts the rest of your life?

This is the moment where most retirees freeze up. You have a 401(k), maybe an IRA, some savings, possibly a pension — and suddenly you need to figure out how much you can spend each month without running out. The stock market is doing its thing. Inflation is chipping away at your purchasing power. And every withdrawal feels like pulling bricks from the foundation of your financial house.

One framework that cuts through the noise better than almost anything else: bucket planning for retirement. It is not complicated. It is not theoretical. And it gives you something that percentages and spreadsheets never can — peace of mind when the market drops 20% and the headlines are screaming.

Table of Contents

- What Is Bucket Planning?

- Bucket 1: The Now Bucket (Years 1-2)

- Bucket 2: The Soon Bucket (Years 3-7)

- Bucket 3: The Later Bucket (Years 8+)

- Setting Up Your Buckets: A Hypothetical Example

- Refilling the Buckets: The Waterfall Strategy

- Bucket Planning and Social Security Coordination

- Common Bucket Planning Mistakes

- Bucket Planning vs. the 4% Rule

- Key Takeaways

- FAQ

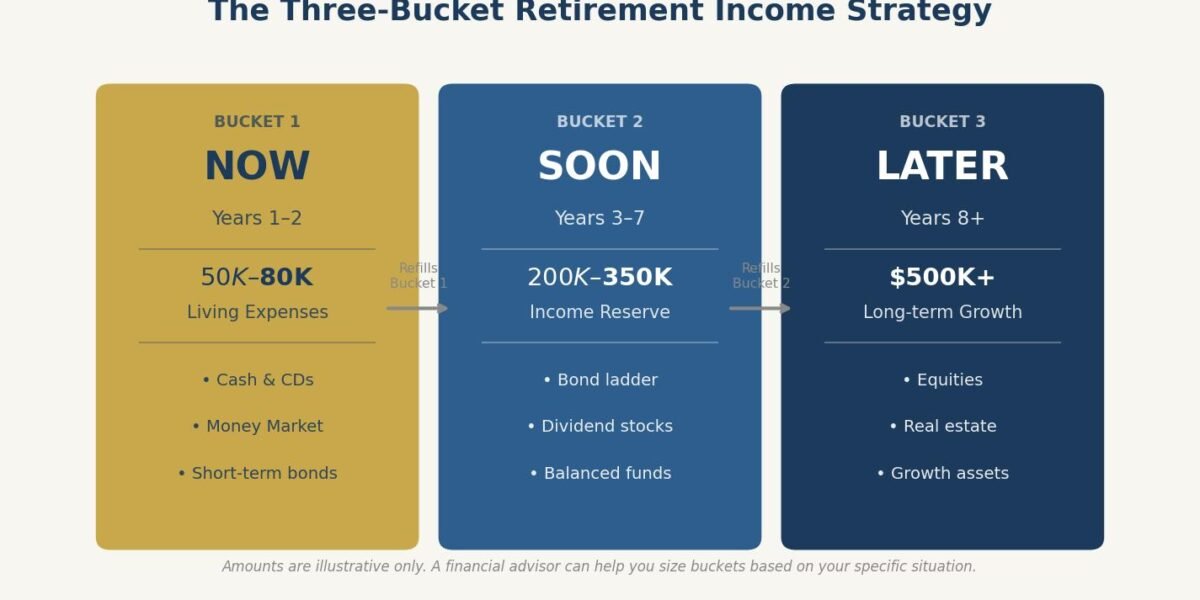

What Is Bucket Planning?

Bucket planning is a retirement income strategy that divides your savings into separate “buckets” based on when you will need the money. Instead of treating your portfolio as one big pool that has to do everything at once — cover your bills today, grow for tomorrow, and survive a market crash — you segment it by time horizon.

The concept was popularized by financial planner Ray Lucia and has been refined by advisors like Harold Evensky, who pioneered the “cash reserve” approach. The core idea is simple: money you need soon should be safe, and money you will not need for years should be invested for growth.

Most bucket strategies use three buckets:

- Bucket 1 (Now): Cash and cash equivalents for immediate living expenses — typically 1 to 2 years of spending

- Bucket 2 (Soon): Conservative investments for medium-term needs — typically years 3 through 7

- Bucket 3 (Later): Growth-oriented investments for long-term needs — year 8 and beyond

This structure addresses the single biggest psychological challenge in retirement: the fear that a market downturn will force you to sell investments at a loss to pay your grocery bill. When you know your next two years of expenses are sitting safely in cash, a bad quarter in the stock market becomes something you can ride out rather than something that keeps you up at night.

Bucket 1: The Now Bucket (Years 1-2)

The Now Bucket is your retirement paycheck. This is the money that covers your day-to-day living expenses for the next one to two years, and it should be completely shielded from market risk.

What goes in Bucket 1:

– High-yield savings accounts

– Money market funds

– Short-term Treasury bills

– Certificates of deposit (CDs) maturing within 12 months

How much belongs here: Enough to cover 12 to 24 months of essential living expenses after accounting for any guaranteed income like Social Security or a pension. If your monthly expenses are $5,000 and Social Security covers $2,500, you need Bucket 1 to hold $30,000 to $60,000 (covering the $2,500 monthly gap for one to two years).

As of early 2026, high-yield savings accounts and short-term Treasuries are still offering yields in the range of 4% to 5%, according to Treasury.gov’s daily rate data. That means your Now Bucket is not just sitting idle — it is earning a reasonable return while providing immediate liquidity.

Thomas’s Take: Many people keep too much in Bucket 1 out of anxiety. Three or four years of cash feels safe, but it creates a drag on your overall portfolio. Two years is the sweet spot for most people — enough to sleep at night, not so much that your money stops working for you.

Bucket 2: The Soon Bucket (Years 3-7)

The Soon Bucket serves as your bridge. It holds investments that are more conservative than stocks but offer better returns than cash. This is the money that will replenish Bucket 1 as you spend it down, and it needs to be stable enough that you are not forced to sell at a loss during a two- to three-year downturn.

What goes in Bucket 2:

– Intermediate-term bond funds (3 to 7 year duration)

– Bond ladder portfolios

– CDs with staggered maturities

– Treasury Inflation-Protected Securities (TIPS)

– Conservative balanced funds (20-30% equity)

How much belongs here: Typically enough to cover years 3 through 7 of spending needs — so roughly three to five years of the gap between your expenses and guaranteed income. Using the same hypothetical as above ($2,500 monthly gap), that would be $90,000 to $150,000.

The purpose of this bucket is to give Bucket 3 time. Stock market downturns, even severe ones, have historically recovered within three to five years. The S&P 500’s historical data shows that even after the 2008 financial crisis — one of the worst downturns in modern history — the market fully recovered within about five and a half years. By the time you are drawing from Bucket 2, Bucket 3 has had years to recover from any downturn.

In-article image: Timeline diagram showing the three buckets across a 20-year retirement horizon, with Bucket 1 covering years 1-2, Bucket 2 covering years 3-7, and Bucket 3 covering year 8 and beyond. Uses TCA navy and gold palette. Alt text: “Timeline showing three retirement income buckets spanning a 20-year horizon with color-coded time segments in navy and gold.”

Bucket 3: The Later Bucket (Years 8+)

The Later Bucket is where your money goes to grow. Because you will not need this money for at least seven to eight years, you can invest it more aggressively and ride out the inevitable ups and downs of the market.

What goes in Bucket 3:

– Diversified stock index funds (domestic and international)

– Growth-oriented mutual funds or ETFs

– Real estate investment trusts (REITs)

– Dividend-growth equities

– Small-cap and mid-cap funds for additional diversification

How much belongs here: Everything that is not in Buckets 1 and 2. For most retirees, this is the largest bucket — typically 50% to 60% of the total portfolio.

The key insight is that with seven-plus years before you need this money, you have recovery time. According to research from J.P. Morgan’s Guide to Retirement, the S&P 500 has never had a negative return over any rolling 20-year period going back to 1950 — and even 10-year periods have been positive the vast majority of the time.

This is also where your portfolio fights inflation. At an average inflation rate of 3%, your purchasing power is cut in half roughly every 24 years. A 25-year retirement that starts comfortable can end painfully if your money is not growing. Bucket 3 is your inflation hedge.

Thomas’s Take: Some retirees move almost everything into bonds and cash on the day they retire. I understand the instinct, but it is one of the most significant risks for a retirement that could last 25 or 30 years. Growth is not optional — it is necessary.

Setting Up Your Buckets: A Hypothetical Example

Let me walk through how bucket planning might look in practice. Consider a hypothetical couple, Jim and Linda, both age 65, retiring with $800,000 in combined savings.

Their situation:

– Monthly living expenses: $5,500

– Combined Social Security (starting at 67): $3,800/month

– No pension

– Current gap to cover from savings: $5,500/month for years 1-2, then $1,700/month after Social Security begins

Their bucket allocation:

| Bucket | Time Horizon | Allocation | Amount | What Is In It |

|---|---|---|---|---|

| Bucket 1 (Now) | Years 1-2 | 16% | $130,000 | High-yield savings, money market, short-term CDs |

| Bucket 2 (Soon) | Years 3-7 | 24% | $190,000 | Intermediate bonds, TIPS, bond ladder |

| Bucket 3 (Later) | Years 8+ | 60% | $480,000 | Diversified stock index funds, REITs, dividend growth |

Why these numbers? For the first two years before Social Security kicks in, Jim and Linda need about $5,500 per month from savings, or $132,000 total. That fills Bucket 1. Once Social Security begins, their monthly gap drops to $1,700. Bucket 2 covers five years of that gap ($102,000) plus a buffer for unexpected expenses, healthcare costs, and inflation adjustments. Everything else goes into Bucket 3 for long-term growth.

This is a hypothetical example for illustrative purposes only and does not represent any actual client situation. Individual circumstances, risk tolerances, and financial goals vary significantly.

In-article image: Allocation pie chart showing Jim and Linda’s $800,000 split across three buckets — 16% Now (gold), 24% Soon (light navy), 60% Later (dark navy) — with dollar amounts labeled. Alt text: “Pie chart showing a hypothetical $800,000 retirement portfolio divided into three buckets: 16% Now, 24% Soon, and 60% Later.”

Refilling the Buckets: The Waterfall Strategy

Setting up your buckets is only half the equation. The real power of bucket planning comes from how you refill them over time — what I call the waterfall strategy.

Free Download: Social Security Optimization Guide

Learn the strategies that could maximize your lifetime Social Security benefits.

Get Your Free CopyHere is how it works:

- Each year, you spend from Bucket 1 to cover your living expenses.

- When Bucket 1 runs low, you replenish it from Bucket 2, selling conservative investments that have (ideally) maintained or grown their value.

- When Bucket 2 runs low, you replenish it from Bucket 3, selling growth investments — but only when markets are favorable.

- If markets are down, you delay replenishing from Bucket 3 and continue drawing from Buckets 1 and 2. This is the entire point of the structure: you have five to seven years of spending covered without ever being forced to sell stocks at a loss.

This waterfall approach also creates natural rebalancing. When stock markets are up significantly, you take some gains off the table by moving money from Bucket 3 to Bucket 2. When markets are flat or down, you leave Bucket 3 alone and let it recover. It is disciplined, systematic, and removes the emotional decision-making that derails so many retirees.

Some advisors build in annual or semi-annual review points — typically in January and July — to assess whether any bucket transfers are needed. I find this rhythm helps clients stay engaged with their plan without obsessing over daily market moves.

Bucket Planning and Social Security Coordination

One of the most powerful applications of bucket planning is coordinating it with your Social Security claiming strategy. The two decisions are deeply connected, and getting them right together can add significantly more income over your retirement than optimizing either one alone.

Consider this: every year you delay Social Security past your full retirement age, your benefit increases by 8% through delayed retirement credits. For many people, delaying from 67 to 70 means a 24% larger benefit — for life, with cost-of-living adjustments built in. That is hard to beat with any investment.

Bucket 1 can serve as a “bridge” that covers your expenses while you delay Social Security to capture those larger benefits. If Jim and Linda from our earlier example could afford to delay Social Security by even two years — using Bucket 1 to bridge the gap — their combined monthly benefit could grow by roughly $600 per month. Over a 20-year retirement, that adds up to more than $144,000 in additional income.

For a deeper look at how the timing of your Social Security claim interacts with your other income sources, I wrote about the most common withdrawal sequencing mistakes in 5 Retirement Withdrawal Mistakes That Cost Thousands. And if you want to understand how spousal benefits factor in, my Complete Guide to Social Security Spousal Benefits covers that in detail.

Thomas’s Take: I think of Bucket 1 as a Social Security delay fund. Using safe, liquid money to bridge the gap while your Social Security benefit grows by 8% per year is one of the most powerful moves in retirement income planning.

Common Bucket Planning Mistakes

Bucket planning is straightforward in concept, but there are several recurring mistakes that undermine it in practice:

1. Keeping too much in Bucket 1. Fear drives people to stockpile three, four, or even five years of cash. Every dollar sitting in cash beyond what you need for the next two years is a dollar not growing. Over 20 years, the opportunity cost is enormous.

2. Never refilling the buckets. Some people set up their buckets and then only spend from Bucket 1 without ever executing the waterfall. Eventually Bucket 1 runs dry, and they are forced to sell from Bucket 3 at whatever the market is doing — exactly the scenario buckets are supposed to prevent.

3. Ignoring taxes in the bucket structure. Which accounts your buckets draw from matters. Pulling from a traditional IRA triggers ordinary income tax. Pulling from a Roth IRA does not. A tax-aware bucket strategy coordinates not just what you sell but where you sell it from. I covered this in detail in How a Couple Saved $18,000 with Roth Conversions.

4. Treating the buckets as rigid. Life changes. Healthcare costs spike. A grandchild needs help with college. The bucket framework should be flexible enough to adapt. Annual reviews are essential — this is a living system, not a set-it-and-forget-it plan.

5. Forgetting about Required Minimum Distributions (RMDs). Starting at age 73 (under current law as of the SECURE 2.0 Act), you must take minimum distributions from traditional retirement accounts. These forced withdrawals need to be factored into your bucket refilling strategy, not treated as an afterthought.

Bucket Planning vs. the 4% Rule

You may have heard of the “4% rule” — the guideline that you can withdraw 4% of your portfolio in year one of retirement and adjust for inflation each year with a high probability of not running out of money over 30 years. It was developed by financial planner William Bengen in 1994 and later validated by the Trinity Study.

Both approaches try to solve the same problem, but they do it differently:

| Factor | Bucket Planning | 4% Rule |

|---|---|---|

| Approach | Segment by time horizon | Single portfolio, fixed withdrawal rate |

| Market downturns | Spend from safe buckets, leave growth alone | Withdraw regardless of conditions |

| Flexibility | Adjusts spending based on bucket levels | Rigid annual withdrawal amount |

| Psychological benefit | High — safe money is visually separate | Lower — all money is in one pool |

| Complexity | Moderate — requires periodic rebalancing | Low — simple percentage calculation |

| Inflation protection | Built into Bucket 3 growth allocation | Inflation adjustment built into rule |

| Sequence-of-returns risk | Mitigated by cash and bond buffers | Vulnerable in early retirement years |

The 4% rule’s biggest vulnerability is sequence-of-returns risk — the danger that a major market downturn in the first few years of retirement permanently impairs your portfolio. Research from Wade Pfau at the American College of Financial Services has shown that poor returns in the first five years of retirement have a disproportionate impact on portfolio longevity.

Bucket planning directly addresses this by ensuring you never sell growth assets during a downturn. Your first five to seven years of spending are already covered by Buckets 1 and 2, giving Bucket 3 time to recover.

That said, the two approaches are not mutually exclusive. Many advisors — myself included — use the 4% rule as a starting point for determining a sustainable spending level, then implement it through a bucket structure. For more on how market conditions affect these strategies, see my article on How to Think About Market Volatility in Retirement.

Key Takeaways

- Bucket planning segments your savings by time horizon — immediate needs in safe assets, medium-term needs in conservative investments, and long-term money in growth investments.

- The framework protects you from sequence-of-returns risk by ensuring you never have to sell stocks during a downturn to pay for groceries.

- Bucket 1 can double as a Social Security bridge, allowing you to delay claiming and capture an 8% annual increase in benefits through delayed retirement credits.

- The waterfall refilling strategy creates natural rebalancing, taking gains when markets are up and leaving growth investments alone when markets are down.

- Annual reviews are essential to adjust for life changes, tax implications, RMDs, and shifting market conditions — buckets are a living system, not a one-time setup.

FAQ

Q: How often should I rebalance my buckets?

Most people benefit from reviewing their bucket allocations once or twice per year. I typically recommend a comprehensive review in January and a lighter check-in mid-year. The goal is to refill Bucket 1 from Bucket 2 as needed, and replenish Bucket 2 from Bucket 3 when market conditions are favorable.

Q: Does bucket planning work if I have a pension?

Absolutely. A pension reduces the amount you need in Bucket 1 because it covers a portion of your monthly expenses with guaranteed income — similar to Social Security. This often means you can allocate more to Buckets 2 and 3, giving your portfolio greater growth potential.

Q: What if the market is down for more than two years — will I run out of Bucket 1?

This is exactly why Bucket 2 exists. Combined, Buckets 1 and 2 typically cover five to seven years of spending. Even the 2008 financial crisis — one of the worst bear markets in history — saw the S&P 500 recover within about five and a half years. Your bucket structure is designed to outlast extended downturns.

Q: Can I use bucket planning with a financial advisor?

Yes, and I would encourage it. A qualified advisor can help you determine the right allocation for each bucket based on your specific income, expenses, tax situation, and goals. Bucket planning is the framework — but the numbers inside each bucket should be personalized to your situation.

Take the Next Step

Turning a lifetime of savings into a reliable retirement income does not have to feel like guesswork. Bucket planning gives you a clear structure, a logical system for spending, and the confidence to ride out market turbulence without panicking. The key is getting the allocations right for your specific situation — your expenses, your income sources, your tax picture, and your timeline.

If you have questions about how bucket planning could work for your retirement, I am always here to help.

Thomas Clark is a Senior Lead Wealth Advisor at Confluence Capital Management, LLC. Investment advisory services offered through Altitude Capital Management, LLC, an SEC-registered investment advisor. Content on this site is for educational and informational purposes only and does not constitute personalized investment advice. Past performance is not indicative of future results. Consult with a qualified financial professional before making any investment decisions.

Thomas Clark is a Series 65 licensed investment advisor and experienced trader. He specializes in investing, retirement planning, and market analysis, helping individuals build wealth and make informed financial decisions.