How to Think About Market Volatility in Retirement

Table of Contents

- Why Market Volatility Feels Different in Retirement

- Sequence-of-Returns Risk Explained Simply

- The Bucket Planning Defense

- Historical Perspective: Every Major Crash in Context

- What NOT to Do When Markets Drop

- What TO Do: A Calm Checklist

- How Much Volatility Can You Actually Afford?

- Building a Volatility-Resistant Retirement Plan

- Key Takeaways

- Frequently Asked Questions

The market dropped 4% last Tuesday. For working investors, market volatility in retirement is just a number on a screen — but if you are retired or close to it, that same 4% probably felt like a punch to the stomach. Many retirees feel the same way: “I know I shouldn’t panic, but this feels different now.”

It does feel different. And there is a real reason for that. When you are drawing income from a portfolio instead of adding to it, a market drop is not just a number on a screen. It is money you may need next month, next year, or in the next decade. The emotional weight of that shift is something no textbook fully prepares you for.

Here is the good news: market volatility in retirement is not something you simply endure. It is something you can plan for, manage, and even use to your advantage. In this guide, I will walk you through why downturns feel so much worse after you stop working, the specific risk that makes early retirement losses particularly impactful, and the concrete strategies that may help keep your income on track no matter what the market does.

Why Market Volatility Feels Different in Retirement

When you were working, every paycheck was a form of defense against market drops. Your 401(k) contributions bought shares at lower prices, and time was on your side. Behavioral economists call this the “accumulation mindset” — losses are temporary because you are still adding fuel to the fire.

Retirement flips that equation. You are now in what researchers call the “decumulation phase,” and the psychology changes dramatically. A 2023 study published in the Journal of Financial Planning found that retirees experience roughly twice the emotional distress from a 10% portfolio decline compared to working-age investors with similar net worth. The reason is straightforward: there are no more paychecks coming to replace what was lost.

There is also a cognitive bias at work called loss aversion — the well-documented tendency for losses to feel about twice as painful as equivalent gains feel good. Nobel laureate Daniel Kahneman’s research showed this effect intensifies when people feel they have fewer opportunities to recover. In retirement, that feeling is not irrational. It is grounded in a real constraint: your time horizon is shorter, and your income sources are more fixed.

Thomas’s Take: The emotional reaction to a market drop in retirement is not weakness — it is your brain correctly recognizing that the stakes have changed. The goal is not to eliminate that feeling. It is to build a plan that keeps you from acting on it.

Sequence-of-Returns Risk Explained Simply

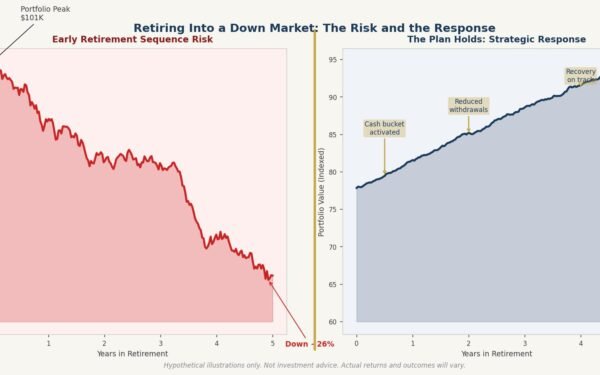

This is the single most important concept for retirees to understand about market volatility, and most people have never heard of it. Sequence-of-returns risk is the danger that poor market returns early in retirement can permanently damage your portfolio — even if long-term average returns are perfectly normal.

Here is a hypothetical example to illustrate. Imagine two retirees, both starting with $1 million and withdrawing $50,000 per year:

| Year | Retiree A Returns | Retiree B Returns |

|---|---|---|

| 1 | -15% | +18% |

| 2 | -10% | +12% |

| 3 | +8% | +6% |

| 4 | +12% | -10% |

| 5 | +18% | -15% |

Both retirees experience the exact same returns — just in reverse order. The average annual return is identical. But after five years of $50,000 withdrawals, Retiree A has approximately $742,000, while Retiree B has approximately $853,000. That is a difference of over $110,000, solely because of the order in which returns arrived.

This is a hypothetical example for illustrative purposes only and does not represent any actual client situation. Actual results would vary based on specific circumstances, fees, and market conditions.

Over a 25- to 30-year retirement, the gap widens significantly. Research from Wade Pfau at the American College of Financial Services suggests that the returns in the first five to seven years of retirement have more impact on portfolio longevity than the returns in any other period.

This is why a broad stock market crash in retirement — particularly in the early years — is a fundamentally different event than the same crash during your working years.

Alt text: Comparison chart showing how identical average returns produce dramatically different outcomes depending on whether losses occur early or late in retirement.

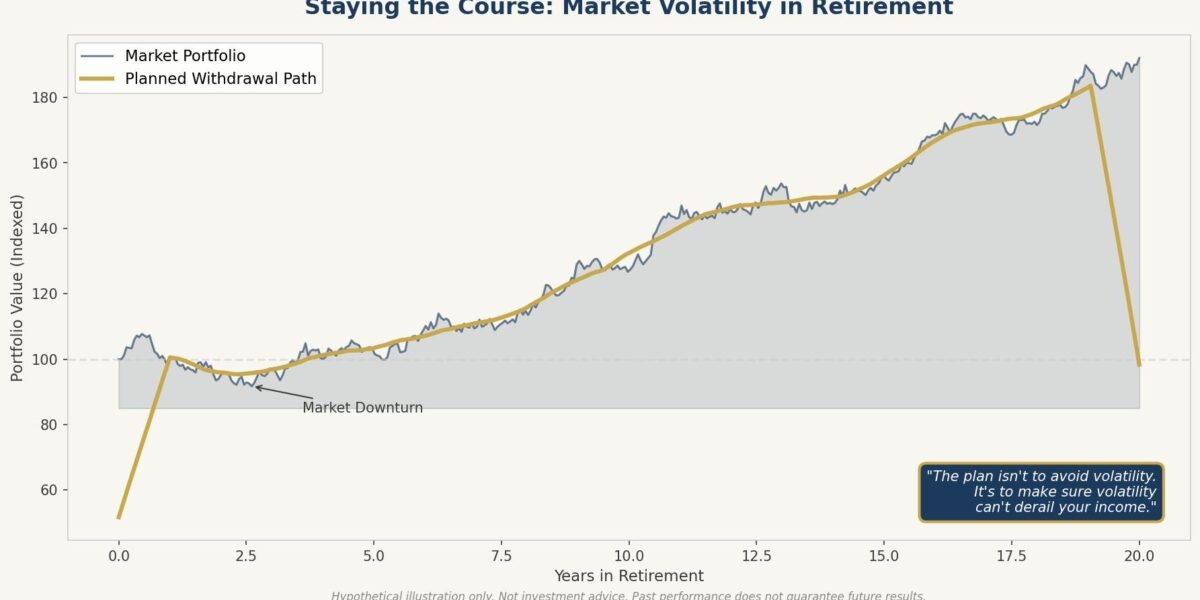

The Bucket Planning Defense

One of the most effective strategies for managing market volatility in retirement is the bucket approach to income planning. This framework is widely used in retirement planning, and it is one of the strategies discussed in detail in my guide on retirement withdrawal mistakes.

The concept is straightforward. Instead of treating your portfolio as one single pool, you divide it into three time-based “buckets”:

Bucket 1: Short-Term (Years 1-3)

- Cash, money market funds, short-term CDs

- Covers 2-3 years of living expenses beyond Social Security and pensions

- This is your “sleep at night” money — it does not fluctuate with the market

Bucket 2: Medium-Term (Years 4-8)

- Bonds, bond funds, balanced funds

- Designed to generate modest growth and income

- Refills Bucket 1 as it is spent down

Bucket 3: Long-Term (Years 9+)

- Diversified stock funds, growth-oriented investments

- This bucket has the longest time horizon and can weather market downturns

- Historically, the stock market has recovered from every major decline given enough time

When the market drops 15% or 20%, you are not selling stocks to pay your electric bill. You are drawing from Bucket 1 — the money that was never in the market to begin with. This separation creates a psychological and financial buffer that may help you ride out downturns without locking in losses.

Historical Perspective: Every Major Crash in Context

Fear thrives in the absence of context. Here is what history actually shows us about major market declines and recoveries:

| Event | Peak Decline | Duration of Decline | Time to Recovery |

|---|---|---|---|

| 1973-74 Oil Crisis | -48% | 21 months | 69 months |

| 1987 Black Monday | -34% | 2 months | 23 months |

| 2000 Dot-Com Bust | -49% | 30 months | 56 months |

| 2007-09 Financial Crisis | -57% | 17 months | 49 months |

| 2020 COVID Crash | -34% | 1 month | 5 months |

| 2022 Inflation Selloff | -25% | 10 months | 22 months |

Source: S&P 500 historical data via Standard & Poor’s. Recovery measured as time to reach previous peak. Past performance is not indicative of future results.

Every single one of these declines recovered fully. Some took months. Some took years. But in every case, investors who stayed the course saw their portfolios come back. The ones who sold at the bottom locked in their losses permanently.

This does not mean the next decline will follow the same pattern. But it does mean that panic-selling has historically been one of the most expensive decisions a retiree could make.

What NOT to Do When Markets Drop

Here are the moves that tend to cause the most damage:

-

Do not sell everything and go to cash. This feels safe, but it locks in your losses and creates a new problem: when do you get back in? Most people who sell in a panic wait too long to reinvest, missing the recovery.

-

Do not check your portfolio every hour. The more frequently you check, the more likely you are to see a loss — and the more likely you are to make an emotional decision. A Vanguard research study found that investors who checked their portfolios daily were significantly more likely to reduce stock allocations at the worst possible time.

Free Download: Social Security Optimization Guide

Learn the strategies that could maximize your lifetime Social Security benefits.

Get Your Free Copy -

Do not make permanent decisions based on temporary conditions. Markets are volatile by nature. A 10% decline happens roughly once per year on average. A 20% decline happens roughly every three to four years. These are not anomalies. They are features of the system.

-

Do not abandon your withdrawal strategy. If you have a plan — particularly a bucket-based approach — now is exactly when it proves its value. Switching strategies mid-downturn is like changing your route during an earthquake.

What TO Do: A Calm Checklist

When markets are falling, here is a checklist that may help you stay grounded:

- Review your Bucket 1 balance. Do you have 2-3 years of expenses in safe, liquid assets? If yes, your short-term income is secure regardless of what the market does today.

- Revisit your withdrawal rate. If you are withdrawing 4% or less of your portfolio annually, research from the Trinity Study and subsequent updates suggests your plan has historically survived most 30-year periods — including those that started with major downturns.

- Look for tax-loss harvesting opportunities. A down market may create opportunities to sell losing positions and offset gains elsewhere. This could be especially relevant if you are managing Roth conversion strategies alongside your regular withdrawals.

- Talk to your advisor. A good conversation about your specific plan during a downturn is worth more than a hundred market predictions.

- Turn off the financial news. Seriously. Cable news is designed to amplify fear because fear drives ratings. Your retirement plan was not built on cable news, and it should not be adjusted by it.

How Much Volatility Can You Actually Afford?

This is the practical question that matters most. The answer depends on several factors:

Your withdrawal rate. The higher your withdrawal rate, the more vulnerable you are to sequence-of-returns risk. A retiree withdrawing 3% of their portfolio can absorb significantly more volatility than one withdrawing 6%.

Your income floor. Social Security, pensions, and annuity income create a “floor” beneath your lifestyle. If your guaranteed income sources cover 70% or more of your essential expenses, your portfolio needs to do less heavy lifting — and can afford to be more aggressive. For a deeper look at how Social Security fits into this picture, see my guide on Social Security spousal benefits.

Your time horizon. A 62-year-old retiree may need their portfolio to last 30+ years. A 78-year-old may need it for 15. The longer your horizon, the more volatility you can generally tolerate — and the more you may actually need stock exposure to outpace inflation.

Your emotional tolerance. This one matters more than most financial models admit. A portfolio allocation that maximizes returns on paper but causes you to panic-sell during the next downturn is not actually optimal. The best allocation is the one you can stick with.

Building a Volatility-Resistant Retirement Plan

No portfolio is immune to market swings. But a well-built retirement plan can absorb those swings without disrupting your income or your peace of mind. Here are the structural elements that matter most:

-

Establish a reliable income floor. Maximize your Social Security benefit by considering your claiming age carefully. Layer in any pensions or guaranteed income sources. The higher your floor, the less your lifestyle depends on market performance.

-

Implement a bucket strategy. Keep 2-3 years of expenses in liquid, low-volatility assets. This is your insulation layer against being forced to sell stocks during a downturn.

-

Diversify beyond stocks. Bonds, Treasury Inflation-Protected Securities (TIPS), and other fixed-income instruments may reduce overall portfolio volatility while providing income. Diversification does not eliminate risk, but it may reduce the severity of any single downturn’s impact.

-

Maintain a flexible withdrawal strategy. Consider reducing withdrawals by 10-15% during major downturns if your budget allows it. Even a small temporary reduction in spending may significantly extend your portfolio’s longevity.

-

Schedule regular plan reviews. Markets change. Your expenses change. Tax laws change. A retirement plan that was built five years ago may need adjustment — not because it was wrong then, but because circumstances evolve.

Key Takeaways

- Market volatility feels different in retirement because it IS different. You are drawing income, not accumulating — and that changes both the math and the psychology.

- Sequence-of-returns risk is the hidden danger. Early losses combined with withdrawals can permanently damage a portfolio, even if long-term returns are strong.

- The bucket strategy creates a buffer. Keeping 2-3 years of expenses in safe assets may help you avoid selling stocks at the worst possible time.

- History favors patience. Every major market decline in the past 50+ years has eventually recovered. Panic-selling has historically been more costly than riding out volatility.

- Your plan should account for volatility before it happens. The time to build a downturn-resilient strategy is before the downturn, not during it.

Frequently Asked Questions

Should I move my retirement portfolio to all bonds or cash during a market crash?

Moving entirely to bonds or cash during a decline locks in your losses and removes the possibility of participating in the recovery. For most retirees, a better approach may be maintaining a diversified allocation and drawing income from safer assets while giving growth-oriented investments time to recover.

How long do stock market crashes typically last?

Based on S&P 500 history, the average bear market (a decline of 20% or more) has lasted roughly 13-14 months. However, individual downturns have ranged from just one month (2020 COVID crash) to 30 months (2000-2002 dot-com bust). Recovery times also vary, but every major decline has eventually been followed by a full recovery.

What is a safe withdrawal rate during a volatile market?

The often-cited “4% rule” suggests that withdrawing 4% of your initial portfolio value, adjusted annually for inflation, has historically survived most 30-year retirement periods. During periods of high volatility, some retirees choose to temporarily reduce withdrawals to 3-3.5% to provide additional margin of safety. Individual situations vary significantly.

Does market volatility mean I should delay my retirement?

Not necessarily. Whether to retire during a volatile market depends on your overall financial picture — including guaranteed income sources, portfolio size, withdrawal rate, and years of expenses in safe assets. A comprehensive retirement income plan that accounts for downturns may allow you to retire on your timeline regardless of short-term market conditions.

Market volatility is not a sign that your retirement plan is broken. It is the price of admission for the long-term growth that helps your money keep pace with inflation over a 25- or 30-year retirement. The retirees who weather downturns best are not the ones who predicted the market correctly — they are the ones who built a plan that did not require them to.

If you have questions about how your current plan holds up against market volatility — or if you would like to explore whether a bucket strategy could work for your situation — I am always here to help.

Thomas Clark is a Senior Lead Wealth Advisor at Confluence Capital Management, LLC. Investment advisory services offered through Altitude Capital Management, LLC, an SEC-registered investment advisor. Content on this site is for educational and informational purposes only and does not constitute personalized investment advice. Past performance is not indicative of future results. Consult with a qualified financial professional before making any investment decisions.

Thomas Clark is a Series 65 licensed investment advisor and experienced trader. He specializes in investing, retirement planning, and market analysis, helping individuals build wealth and make informed financial decisions.