Karen just turned 64, and she has a problem most people would envy: she loves her job. As a senior project manager at a mid-size technology firm, she has excellent employer health insurance, a salary she is proud of, and zero desire to retire anytime soon. But her 65th birthday is nine months away, and the Medicare enrollment letters have already started arriving.

Her question about Medicare while still working is one many pre-retirees face: “If I have good insurance through work, do I actually need to sign up for Medicare when I turn 65?” The answer is not as simple as yes or no — and getting it wrong could cost thousands of dollars in penalties or coverage gaps that follow you for the rest of your life.

In this article, I will walk through Karen’s situation as a hypothetical case study to illustrate the key decision points, hidden traps, and financial considerations that anyone working past 65 should understand. This is a hypothetical example for illustrative purposes only and does not represent any actual client situation.

Table of Contents

- The Core Decision: Employer Coverage vs. Medicare

- Running the Numbers: A Side-by-Side Comparison

- The Part B Late Enrollment Penalty Trap

- Part D Considerations: The Creditable Coverage Rule

- The HSA Complication Most People Miss

- Medicare While Still Working: Karen’s Decision Framework

- What Karen Decided and Why

- Key Takeaways

- Frequently Asked Questions

The Core Decision: Employer Coverage vs. Medicare

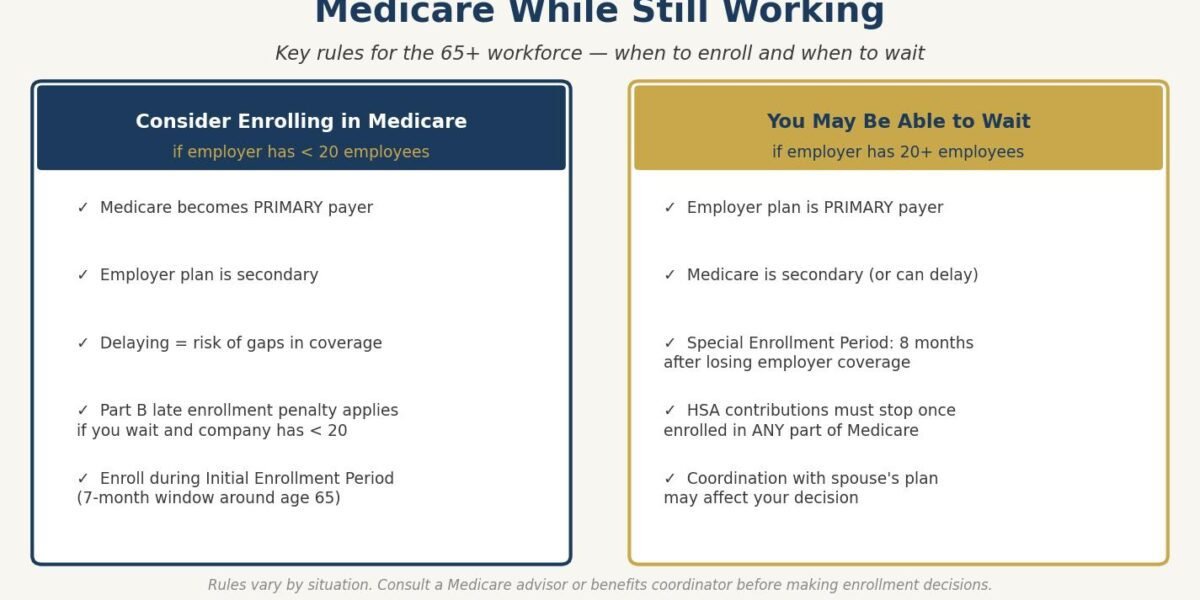

The first thing Karen needs to determine is the size of her employer. This single fact changes everything about her Medicare decision, and it is the first question to determine.

The 20-employee rule: If your employer has 20 or more employees, your employer’s group health plan is the “primary payer” — meaning it pays first, and Medicare would be secondary. In this scenario, you are generally not required to enroll in Medicare Part B at 65, and you will not face a late enrollment penalty when you eventually do sign up, as long as you had continuous employer coverage.

If your employer has fewer than 20 employees, Medicare becomes the primary payer at 65 regardless of whether you have employer coverage. In that case, delaying Medicare enrollment could leave you with significant coverage gaps and penalties.

Karen’s company has about 200 employees, so she falls squarely in the 20-or-more category. This gives her a genuine choice. But that does not mean she should automatically skip Medicare. According to Medicare.gov, understanding your employer size and coverage type is the critical first step.

What about Part A? Most people are eligible for premium-free Medicare Part A (hospital insurance) at 65 if they or their spouse paid Medicare taxes for at least 10 years. Because Part A is free for most people, it might seem like a no-brainer to enroll. And for many people, it is. But there is a significant exception I will cover in the HSA section below that could make enrolling in Part A a costly mistake.

Running the Numbers: A Side-by-Side Comparison

Karen asked me to lay out the costs, so let us look at a hypothetical comparison between her current employer plan and what Medicare would cost her. These are illustrative figures based on typical 2026 costs.

| Coverage Element | Employer Plan (Hypothetical) | Medicare (Hypothetical) |

|---|---|---|

| Monthly premium | $280 (employee share) | $202.90 (Part B) + $35 (Part D) + $175 (Medigap Plan G) = $412.90 |

| Annual deductible | $1,500 | $283 (Part B) + $1,676 (Part A per benefit period) |

| Out-of-pocket max | $5,000 | Varies by Medigap plan; Plan G covers most gaps |

| Prescription coverage | Included | Part D plan required (separate premium + formulary) |

| Dental/Vision | Included | Not covered by Original Medicare |

| Network restrictions | PPO — broad network | Any provider accepting Medicare — very broad |

Note: All figures are hypothetical estimates for illustrative purposes. Actual costs vary by location, plan, and individual circumstances. Source: CMS.gov 2026 Medicare costs. For a full breakdown of 2026 premium and IRMAA changes, see my article on 2026 Medicare changes every pre-retiree must know.

For Karen, her employer plan currently costs her less per month with broader benefits including dental and vision. On paper, keeping the employer plan looks like the better financial deal — at least while she is working and her employer is subsidizing the premium.

But the monthly premium is only one piece of the puzzle. The real question is what happens when she eventually leaves her job.

Thomas’s Take: It may help to think of this decision on two timelines — not just what is cheaper today, but what protects you best when you transition. The enrollment rules and penalty structures make the “when you leave” part just as important as the “while you are working” part.

The Part B Late Enrollment Penalty Trap

This is where the stakes get real. Medicare Part B has a late enrollment penalty that is permanent — it never goes away.

If you do not sign up for Part B during your Initial Enrollment Period (the seven-month window around your 65th birthday) and you do not qualify for a Special Enrollment Period, Medicare adds a 10% surcharge to your Part B premium for every full 12-month period you could have had Part B but did not. That penalty is added to your premium for as long as you have Medicare.

Here is the good news for Karen: because her employer has 20 or more employees and she has active employer coverage, she qualifies for a Special Enrollment Period (SEP) when her employer coverage ends. This SEP gives her eight months after her employment ends or her coverage stops (whichever comes first) to sign up for Part B without a penalty.

According to SSA.gov, the SEP is specifically designed for people in Karen’s situation — but you must be able to document that you had continuous employer group health plan coverage.

The trap catches people who work for small employers (fewer than 20 employees) or who have COBRA or retiree coverage — neither of which qualifies for the SEP. COBRA and retiree health plans are not considered active employer coverage by Medicare. It is not uncommon for people who retired at 65 and elected COBRA thinking they were protected, only to face permanent penalties when they tried to enroll in Part B a year or two later.

Pro Tip: If you are delaying Part B because of employer coverage, get a letter from your employer’s HR department confirming your group health plan coverage start and end dates. You will need this documentation (CMS form L564) when you eventually enroll. Do not wait until you need it — get it while you are still employed and HR can easily provide it.

Part D Considerations: The Creditable Coverage Rule

Medicare Part D (prescription drug coverage) has its own separate penalty structure, and it hinges on a concept called creditable coverage.

Creditable coverage means your current prescription drug plan is at least as good as a standard Medicare Part D plan. Your employer is required to send you a notice each year — usually in the fall — telling you whether your employer drug coverage is creditable or not.

If Karen’s employer drug coverage is creditable, she can delay enrolling in Part D without penalty. When she eventually leaves her job, she will have a 63-day window to enroll in a Part D plan without a late penalty.

If her employer coverage is not creditable (which is rare for large-employer plans but does happen), she would face a Part D late enrollment penalty of roughly 1% of the national base beneficiary premium for each month she went without creditable coverage. In 2026, that base premium is approximately $36.78, so every month without creditable coverage adds about $0.37 per month to her premium — permanently. A three-year gap could mean an extra $13 or more per month for life. Details are available at Medicare.gov Part D late penalty information.

Karen checked her annual notice and confirmed that her employer’s drug coverage is creditable. She filed that notice away — and I recommend everyone does the same.

Free Download: Social Security Optimization Guide

Learn the strategies that could maximize your lifetime Social Security benefits.

Get Your Free CopyThe HSA Complication Most People Miss

Here is the surprise that catches many people working past 65 off guard: if you enroll in Medicare Part A, you can no longer contribute to a Health Savings Account (HSA).

Karen has been contributing the maximum to her HSA for years. In 2026, the family contribution limit is $8,550 (with a $1,000 catch-up for those 55 and older), giving her $9,550 in pre-tax savings annually. That is a significant tax benefit she does not want to lose.

The issue is that Medicare Part A enrollment can be retroactive. If you sign up for Part A after age 65, the Social Security Administration can backdate your Part A coverage up to six months. If that retroactive coverage overlaps with any months you contributed to your HSA, you could face tax penalties and need to withdraw those contributions.

There is another wrinkle: if you are already receiving Social Security benefits, you are automatically enrolled in Part A at 65. There is no opting out. This means people who claimed Social Security early (at 62, for instance) and are still working at 65 will lose their HSA contribution eligibility when Part A kicks in automatically.

Karen is not receiving Social Security yet, so she has a choice. By delaying Part A enrollment along with Part B, she can continue her HSA contributions. For someone in the 25% tax bracket contributing $9,550 annually, that is roughly $2,388 in tax savings each year — a meaningful number that should factor into the overall decision.

Medicare While Still Working: Karen’s Decision Framework

After we laid out all the factors, Karen’s decision came down to answering four key questions:

1. Is my employer coverage genuinely good?

Yes. Her plan has lower premiums than Medicare would cost, includes dental and vision, and covers her preferred doctors. For the coverage quality alone, staying on her employer plan makes sense while she is working.

2. Am I contributing to an HSA?

Yes, and the tax savings are significant. Enrolling in even premium-free Part A would end those contributions. Since her employer plan provides strong coverage, delaying both Part A and Part B preserves her HSA benefit.

3. Do I understand the timeline when I leave?

This is the critical planning piece. Karen now knows she has an eight-month Special Enrollment Period after her employer coverage ends to sign up for Part B without penalty. She also knows she needs the employer documentation ready, and she has 63 days for Part D.

4. What is my backup plan if I lose my job unexpectedly?

This is the question many people skip. If Karen were laid off or her company changed insurance plans, she needs to act quickly. Having a Medicare enrollment checklist ready — including the employer coverage documentation — means she will not be scrambling during a stressful transition. For more on retirement income planning during unexpected transitions, see my article on bucket planning for retirement income.

What Karen Decided and Why

Karen decided to delay all Medicare enrollment — Part A, Part B, and Part D — while she continues working with her current employer coverage. Here is her reasoning:

- Cost savings: Her employer plan costs $280 per month compared to an estimated $413 or more for Medicare with a Medigap supplement, and it includes dental and vision that Medicare does not cover.

- HSA preservation: Continuing her HSA contributions saves her approximately $2,388 per year in taxes, and the account balance will grow tax-free for future healthcare costs in retirement.

- No penalty risk: With 200+ employees, her employer plan qualifies her for the Special Enrollment Period, so she will face zero penalties when she eventually enrolls.

- Creditable drug coverage: Her employer’s prescription coverage is creditable, protecting her from Part D penalties as well.

She also created a “Medicare activation plan” with these steps for when she eventually leaves her employer:

1. Request form CMS-L564 from HR (proof of employer coverage)

2. Contact Social Security to start Part A and Part B enrollment

3. Research and select a Medigap plan during her one-time open enrollment

4. Enroll in a Part D prescription drug plan within 63 days

5. Stop HSA contributions the month Part A coverage begins

Karen’s decision was right for her situation. But it would have been the wrong decision if her employer had fewer than 20 employees, if she were already receiving Social Security, or if her employer plan was not creditable for drug coverage. That is why the framework matters more than any single answer.

For a broader look at how healthcare decisions fit into your overall retirement income plan, see my guide on how the 2026 tax bracket changes affect retirees.

Key Takeaways

- Employer size is the threshold question. If your employer has 20 or more employees, you generally can delay Medicare without penalty while you have active employer coverage. Under 20 employees, Medicare becomes primary and delaying is risky.

- Part B penalties are permanent. A 10% surcharge for every 12-month period you could have enrolled but did not — and it never goes away. Make sure you qualify for the Special Enrollment Period before delaying.

- HSA contributions and Medicare Part A cannot coexist. If you are maximizing HSA contributions and do not need Part A coverage, delaying Part A enrollment could save thousands in tax benefits.

- Document everything while you are still employed. Get proof of employer coverage (form CMS-L564) and save your annual creditable coverage notices. You will need these when you eventually enroll.

Frequently Asked Questions

Can I have both employer insurance and Medicare at the same time?

Yes, you can enroll in Medicare while still covered by your employer plan. If your employer has 20 or more employees, the employer plan pays first (primary) and Medicare pays second (secondary). Some people do this to reduce out-of-pocket costs, particularly if they have high medical expenses. However, the additional Medicare premiums may not be worth it if your employer plan already provides strong coverage.

What if my employer has exactly 20 employees?

The 20-employee threshold is based on the number of employees the company had for 20 or more calendar weeks in the current or preceding year, according to CMS.gov. If your employer meets that threshold, the employer plan is primary. If you are unsure, ask your HR department directly and request written confirmation of how many employees are counted for Medicare coordination purposes.

What happens if I miss the eight-month Special Enrollment Period after leaving my job?

If you miss the eight-month SEP after your employer coverage ends, you would need to wait for the General Enrollment Period, which runs from January 1 through March 31 each year, with coverage starting July 1. During that gap, you could be without Part B coverage and would face the permanent late enrollment penalty. This is why having a Medicare activation plan before you leave your employer is so important.

The decision to enroll in Medicare while still working is one of the most consequential healthcare choices you will make — and it is far more nuanced than most people realize. The right answer depends entirely on your employer size, your current benefits, your HSA strategy, and your timeline.

If you have questions about how Medicare enrollment fits into your overall retirement plan, schedule a complimentary consultation — I am always here to help.

Thomas Clark is a Senior Lead Wealth Advisor at Confluence Capital Management, LLC. Investment advisory services offered through Altitude Capital Management, LLC, an SEC-registered investment advisor. Content on this site is for educational and informational purposes only and does not constitute personalized investment advice. Past performance is not indicative of future results. Consult with a qualified financial professional before making any investment decisions.

Thomas Clark is a Series 65 licensed investment advisor and experienced trader. He specializes in investing, retirement planning, and market analysis, helping individuals build wealth and make informed financial decisions.