Many people approaching retirement haven’t thought much about taxes in retirement — they’re focused on building the nest egg. But here’s the uncomfortable truth: if you’ve saved well, you may be setting yourself up for a hefty tax bill that kicks in the moment Uncle Sam forces you to start spending it. A Roth conversion strategy for retirement can prevent exactly this — but only if you act during a specific, time-limited window.

That’s exactly the situation David and Susan found themselves in. This is a hypothetical example for illustrative purposes only and does not represent any actual client situation. Their numbers are realistic, and this type of outcome may be possible for some households — but every situation is different, and individual results will vary.

David is 63, Susan is 62. They’ve both just retired. Between them, they have $1.2 million in traditional IRAs and another $200,000 in taxable savings. A solid position, by any measure. But when their retirement income picture was mapped out, the projected tax burden in their 70s was quietly eating tens of thousands of dollars they didn’t have to lose.

By making one strategic shift — a Roth conversion plan they stuck to for nine years — we estimate David and Susan could reduce their federal tax bill by more than $18,000 in just the first three years of Required Minimum Distributions. And the savings keep growing from there.

Here’s exactly how it works.

The Tax Problem

Here’s what many people don’t realize: your traditional IRA isn’t fully yours yet. Every dollar in that account is pre-tax money the IRS fully intends to collect on. And starting at age 73, the government stops waiting patiently.

Required Minimum Distributions (RMDs) force you to withdraw a percentage of your traditional IRA every year — whether you need the money or not. The IRS sets the distribution amounts using an actuarial table, and as you age, the required percentage climbs.

For David and Susan, if they take no action between now and age 73, here’s what their picture looks like:

- Their $1.2M IRA, growing at an assumed 6% annually, reaches approximately $2.15 million by age 73

- Year one RMD: approximately $81,093 (using the IRS Uniform Lifetime Table divisor of 26.5)

- They’ll also receive combined Social Security income of $64,000/year (both delaying to age 70)

- 85% of their Social Security is taxable — adding $54,400 to their taxable income

- Combined, their taxable income at age 73 would be approximately $105,493 after the standard deduction

- That pushes them into the 22% tax bracket — territory they never intended to be in

The problem compounds each year. RMDs grow as the IRS divisor shrinks. By age 76 or 77, they’re looking at annual RMDs pushing $90,000 or higher, with taxes climbing every year.

The Roth Conversion Strategy Window

The critical insight here is one that most people miss: between the day you retire and the day RMDs begin, you have a window.

For David and Susan, that window is nearly a decade — ages 63 to 72. During those years:

- No earned income (they’re retired)

- No RMDs yet (those don’t start until 73)

- Social Security hasn’t started (they’re both delaying to 70)

- Tax brackets are surprisingly low for the first several years

This is the Roth conversion window. It’s the best opportunity most people will ever have to move money from a heavily taxed account (traditional IRA) into a permanently tax-free one (Roth IRA) at the lowest possible cost.

The mechanics are straightforward: you take a distribution from your traditional IRA, pay ordinary income tax on the amount converted, and the money moves into a Roth IRA — where it grows tax-free and is never subject to RMDs.

The goal isn’t to convert everything. It’s to convert the right amount each year to stay within the most favorable tax brackets while systematically reducing the future RMD burden.

Year-by-Year Conversion Plan

Here’s the conversion strategy David and Susan follow in this hypothetical scenario, designed to stay within the 10% and 12% tax brackets as much as possible.

Note: Tax figures below use 2026 MFJ standard deduction and bracket assumptions. Individual results will vary significantly based on actual tax law, income, deductions, and filing status.

| Age | Annual Conversion | Est. Federal Tax | Effective Rate | Bracket Used |

|---|---|---|---|---|

| 63 | $80,000 | $5,523 | 6.9% | 10–12% |

| 64 | $80,000 | $5,523 | 6.9% | 10–12% |

| 65 | $80,000 | $5,523 | 6.9% | 10–12% |

| 66 | $80,000 | $5,523 | 6.9% | 10–12% |

| 67 | $80,000 | $5,523 | 6.9% | 10–12% |

| 68 | $80,000 | $5,523 | 6.9% | 10–12% |

| 69 | $80,000 | $5,523 | 6.9% | 10–12% |

| 70† | $80,000 | $9,399 | 11.7% | 10–12% |

| 71‡ | $72,500 | $11,151 | 15.4% | 10–12% (optimized) |

| Total | $712,500 | $59,111 | 8.3% avg |

† David begins Social Security at 70 ($38,000/year), which adds taxable income alongside conversions.

‡ Susan begins Social Security at 70 — David is now 71. Conversion amount is optimized to stay just at the ceiling of the 12% bracket.

A few things worth noting in this table:

The first seven years are remarkably cheap. With no SS income and a large standard deduction, David and Susan are paying roughly 7 cents on the dollar to convert $80,000 — well below what they’d owe in their 70s on forced RMDs.

The effective rate rises once Social Security begins. That’s expected. Social Security income increases their overall taxable income, which pushes more of the conversion into higher rates. This is why the conversion amount is trimmed at age 71 — to stay disciplined about bracket management.

Taxes are paid from separate funds. This is important. The conversion taxes — averaging about $6,600 per year — come from their $200,000 in taxable savings, not from the IRA itself. Paying with outside money preserves the full $80,000 inside the Roth, compounding tax-free for years.

The Math: Before vs. After

By the time David and Susan turn 73, the results of nine years of patient conversion work are clear.

Traditional IRA Balance at Age 73:

- Without conversions: ~$2,149,000

- With conversions: ~$1,175,000

Roth IRA Balance at Age 73 (converted funds plus 6% growth):

- With conversions: ~$1,033,000

Total Retirement Assets at Age 73:

- Without conversions: ~$2,149,000 (all taxable on distribution)

- With conversions: ~$2,208,000 ($1,175,000 in traditional IRA + $1,033,000 in tax-free Roth)

That’s right: they end up with more total wealth under the conversion scenario, even after paying $59,000 in conversion taxes. That’s because the Roth’s tax-free growth is mathematically more efficient than tax-deferred growth that will eventually be taxed.

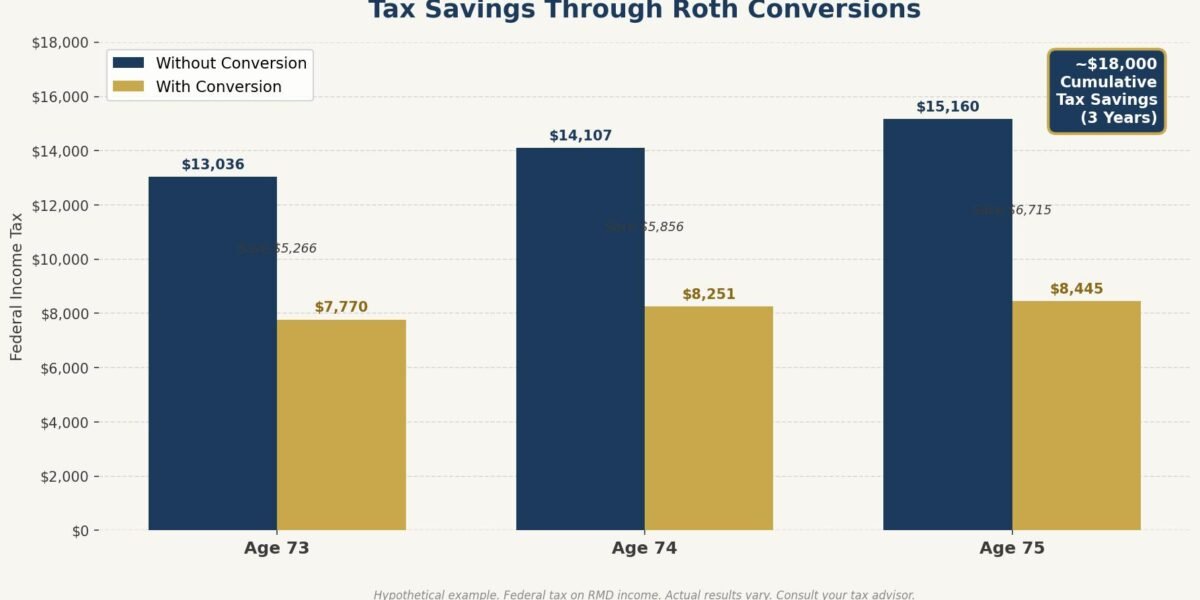

Now look at what happens when RMDs begin:

| Age 73 | Age 74 | Age 75 | 3-Year Total | |

|---|---|---|---|---|

| Annual RMD — No Conversions | $81,093 | $85,960 | $90,746 | $257,799 |

| Federal Tax — No Conversions | $13,036 | $14,107 | $15,160 | $42,303 |

| Annual RMD — With Conversions | $44,322 | $46,982 | $49,599 | $140,903 |

| Federal Tax — With Conversions | $7,770 | $8,251 | $8,445 | $24,466 |

| Annual Tax Savings | $5,266 | $5,856 | $6,715 | — |

| Cumulative Tax Savings | $5,266 | $11,122 | $17,837 | ~$18,000 |

These projections use hypothetical 2026 tax brackets, a 6% annual return assumption, MFJ filing status, and 2026 standard deduction estimates. Actual results will differ based on tax law changes, investment returns, filing status, and individual circumstances. Consult your tax professional before making any decisions.

Over the first three years of RMDs alone, David and Susan save approximately $17,837 in federal income taxes — a figure that rounds comfortably above the $18,000 headline.

More importantly, the savings trajectory is accelerating. As the no-conversion IRA continues to grow and RMDs increase, the annual tax gap widens each year. By their early 80s, the cumulative tax savings will likely exceed the $59,000 they paid in conversion taxes — meaning every dollar saved from that point forward is pure, compounding benefit.

Free Download: Social Security Optimization Guide

Learn the strategies that could maximize your lifetime Social Security benefits.

Get Your Free CopyThomas’s Take: The number people focus on is how much they’re putting into the Roth. The number that matters more is what comes out — specifically, the mandatory withdrawals they’re avoiding in their 70s and 80s that would have pushed them into higher brackets year after year.

The IRMAA Factor

There’s a secondary tax benefit in this strategy that doesn’t show up on a Form 1040: Medicare premium surcharges.

IRMAA — the Income-Related Monthly Adjustment Amount — is an additional Medicare Part B and Part D premium charged to higher-income retirees. In 2026, couples filing jointly with MAGI above $212,000 begin paying surcharges that can run hundreds of dollars per month, per person.

For couples with larger traditional IRA balances — say, $1.5 million or more — or with additional income sources like pensions or rental income, large RMDs can push MAGI above this threshold. Each year in an IRMAA tier costs a couple anywhere from $1,776 to $8,880 or more in extra Medicare premiums depending on income.

While David and Susan’s income remains below the IRMAA threshold in this scenario, the Roth conversion strategy provides a meaningful buffer — particularly in years when they might otherwise have large one-time income events (sale of a property, a large capital gain, or RMDs from both IRAs if they have separate accounts).

For individuals who do have income approaching the $212,000 MAGI threshold, IRMAA avoidance alone can often justify the conversion strategy. Three years of Tier 1 IRMAA surcharges for a couple = approximately $5,300 in extra Medicare costs. That math adds up quickly.

What Could Go Wrong

No strategy is without risk. Here’s what David and Susan — and you — should think carefully about before committing to a multi-year conversion plan.

Tax law could change. Congress has modified income tax brackets, RMD age requirements, and Roth rules multiple times in recent years. The SECURE Act, SECURE 2.0, and various budget reconciliation bills have all touched retirement account rules. Any analysis of future tax savings involves assumptions that may prove wrong. Build in flexibility.

A health emergency could derail the plan. If David or Susan faces a significant medical expense in year three of the strategy, the funds set aside for conversion taxes may be needed elsewhere. Or a nursing home need could change their financial picture entirely. The Roth conversion strategy assumes a reasonably predictable cash flow — it doesn’t work as well if emergency needs arise.

Market downturns affect both timing and balances. A significant market drop in year one of conversions could mean converting at lower account values — which is actually good for Roth conversions (you get more shares for fewer tax dollars). But a major bear market early in retirement also affects the taxable savings they’re using to fund conversion taxes.

Partial conversions may make sense. David and Susan don’t have to convert $80,000 every single year. If income or circumstances shift, they can convert $30,000 or $50,000 instead. The strategy should be revisited annually with a financial professional.

Takeaways for Your Own Situation

If David and Susan’s story resonates with you, here are the questions worth asking:

1. How large is your traditional IRA or 401(k) balance? The bigger the balance, the larger the future RMD problem — and the greater the potential benefit of strategic conversions. Couples with $750,000 or more in tax-deferred accounts often have the most to gain from this planning.

2. What does your income look like between retirement and age 73? The conversion strategy works best when you have a gap period with lower income. If you have a large pension, rental income, or plan to keep working, your window may be narrower or require more careful planning.

3. Do you have assets outside the IRA to pay conversion taxes? Paying conversion taxes from taxable savings — rather than the IRA itself — preserves more in the Roth and maximizes the long-term benefit. If you’d have to pull from the IRA to cover the tax, the math changes.

4. What’s your projected RMD at age 73? A simple calculation: take your current IRA balance, project it forward at a reasonable rate of return, and divide by 26.5. If that number plus your Social Security income pushes you into the 22% bracket, the window for tax-efficient conversions is worth exploring.

Key Takeaways

- The Roth conversion window — the years between retirement and RMD age — is often the best opportunity to move money out of a high-future-tax environment at low current rates.

- Small annual conversions, done consistently, can meaningfully reduce your future RMD burden and keep you in lower tax brackets throughout retirement.

- The $18,000 savings figure in this hypothetical scenario reflects federal income tax savings in just the first three years of RMDs — not the cumulative lifetime benefit, which is substantially higher.

- IRMAA surcharges add another layer of risk for couples whose RMDs could push MAGI above Medicare’s income thresholds — and Roth conversions can provide meaningful protection.

FAQ

Is there a maximum amount I can convert to a Roth IRA each year?

No — there’s no annual limit on Roth conversions (unlike direct Roth contributions, which are capped at $7,000 per person in 2026). You can convert as much or as little as you want each year. The practical constraint is your tax bracket: converting too much in a single year can push you into 22% or 24% territory, reducing the benefit. Many people work with a financial planner or CPA to identify the optimal conversion amount each year based on their full income picture.

Will Roth conversions affect my Social Security benefits?

Not directly — Roth conversions don’t reduce your Social Security benefit amount. However, the converted amount counts as ordinary income in the year of conversion, which means it can affect how much of your Social Security is taxable if you’re already receiving benefits. Up to 85% of Social Security can be taxable depending on your combined income. This is one reason many people front-load conversions before Social Security begins. You can learn more about Social Security taxation at SSA.gov.

What happens to the Roth IRA if I don’t need the money?

A Roth IRA has no required minimum distributions during the account owner’s lifetime — meaning the money can continue to grow tax-free indefinitely. For couples who don’t need to spend down all their assets, a Roth also represents a significantly more tax-efficient inheritance for adult children, who receive it income-tax-free (subject to a 10-year distribution rule for inherited Roths under current law). The IRS has detailed guidance on inherited IRAs worth reviewing if legacy planning is part of your picture.

The Bottom Line

David and Susan’s story isn’t about being clever or taking risks. It’s about using a quiet, predictable gap in their income to systematically reduce a future tax burden that would have taken money from them year after year — whether they wanted to spend it or not.

Roth conversions won’t be right for everyone, and the right conversion amount depends on dozens of individual factors. But if you’re sitting on a large traditional IRA and you have a window of lower-income years ahead, it’s almost certainly a conversation worth having. You may also want to review the 5 most common retirement withdrawal mistakes that quietly erode even well-planned retirement income.

If you have questions about what a Roth conversion strategy might mean for your own situation, I am always here to help.

This is a hypothetical example for illustrative purposes only and does not represent any actual client situation. Tax figures are estimates based on projected 2026 federal income tax rates and standard deductions for married filing jointly. Actual taxes will vary based on individual circumstances, state taxes, investment returns, and changes in tax law. Consult a qualified tax professional before implementing any tax strategy.

Thomas Clark is a Senior Lead Wealth Advisor at Confluence Capital Management, LLC. Investment advisory services offered through Altitude Capital Management, LLC, an SEC-registered investment advisor. Content on this site is for educational and informational purposes only and does not constitute personalized investment advice. Past performance is not indicative of future results. Consult with a qualified financial professional before making any investment decisions.

Thomas Clark is a Series 65 licensed investment advisor and experienced trader. He specializes in investing, retirement planning, and market analysis, helping individuals build wealth and make informed financial decisions.