The 2026 Medicare changes are already affecting retirees’ wallets. Your Part B premium jumped nearly ten percent, and if you are planning to retire in the next few years, that single line item could mean an extra $215 out of your pocket annually — and that is before we even talk about the income-related surcharges that catch many higher-earning pre-retirees off guard.

The good news? Not every 2026 Medicare change is a cost increase. A new prescription drug spending cap, negotiated drug prices, and tighter rules on Medicare Advantage prior authorizations could put real money back in your pocket, if you know how to plan around them.

Here is what changed for 2026, what it actually means for your retirement budget, and three steps you can take right now to prepare.

Table of Contents

- Part B Premiums and Deductibles: The Numbers

- Part D Prescription Drug Updates

- IRMAA Bracket Changes for 2026

- Medicare Advantage: What Is Changing

- What This Means If You Are Retiring in 2026

- Three Steps to Take Now

- Key Takeaways

- FAQ

Part B Premiums and Deductibles

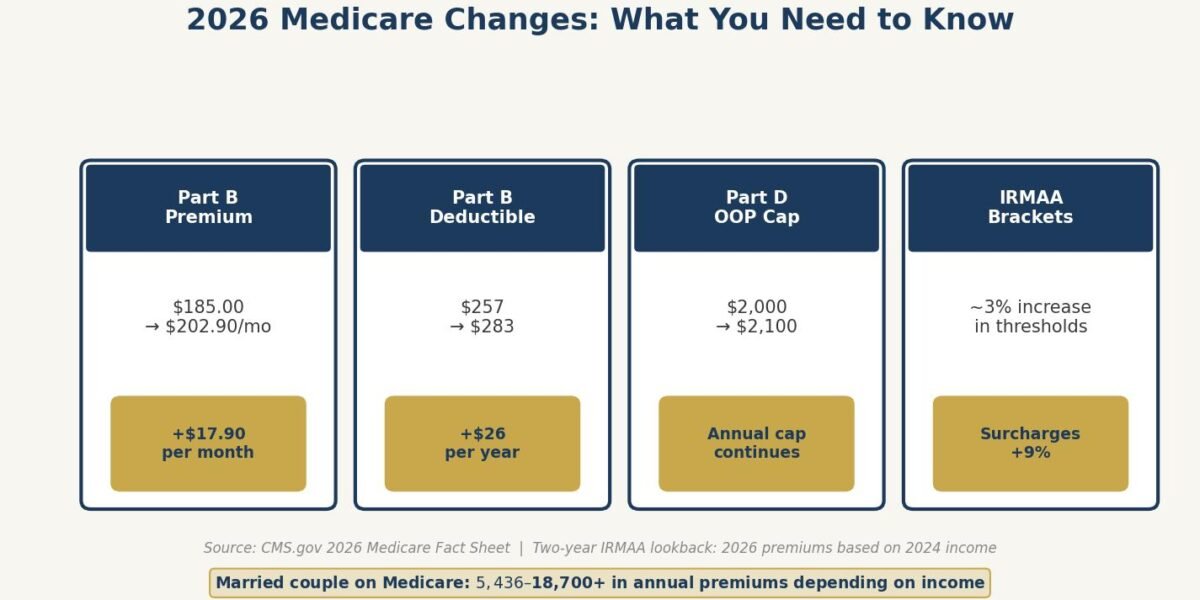

The standard monthly premium for Medicare Part B rose to $202.90 in 2026, up from $185.00 in 2025. That is a $17.90 per month increase, or about $215 more per year.

The annual Part B deductible also climbed to $283, up $26 from the $257 deductible in 2025.

| Cost Category | 2025 | 2026 | Change |

|---|---|---|---|

| Part B Monthly Premium | $185.00 | $202.90 | +$17.90/mo |

| Part B Annual Deductible | $257 | $283 | +$26/yr |

| Total Annual Part B Cost | $2,477 | $2,717.80 | +$240.80/yr |

According to CMS, the increase reflects projected price changes and utilization trends consistent with historical experience. CMS also noted that the premium increase would have been about $11 more per month had the administration not addressed unprecedented spending on skin substitute products through the 2026 Physician Fee Schedule Final Rule.

Thomas’s Take: For a married couple both on Medicare, this premium increase alone adds roughly $430 to your annual healthcare budget. If you are building a retirement income plan, make sure your projections account for Medicare cost inflation of five to eight percent annually, not just general inflation.

Part D Prescription Drug Updates

The biggest positive change in recent Medicare history continues to unfold. Thanks to the Inflation Reduction Act, Medicare Part D now includes an annual out-of-pocket spending cap, which was a first when it took effect in 2025.

For 2026, that cap has been adjusted to $2,100, up from $2,000 in 2025. The increase reflects the annual percentage change in average Part D drug expenditures, as outlined by CMS.

Here is how the Part D benefit structure works in 2026:

- Deductible phase — You pay the full cost of covered drugs until you meet your plan’s deductible (varies by plan).

- Initial coverage phase — You pay 25% coinsurance for covered drugs.

- Catastrophic coverage — Once your out-of-pocket spending reaches $2,100, you pay nothing for covered Part D drugs for the rest of the year.

Additionally, Medicare’s drug price negotiation program continues to expand. CMS has negotiated prices on an initial set of high-cost drugs that took effect in 2026, with 15 additional drugs selected for future negotiation rounds.

The Medicare Prescription Payment Plan also remains available, allowing beneficiaries to spread their out-of-pocket prescription costs across monthly payments throughout the year rather than paying large amounts upfront.

Pro Tip: If you take expensive brand-name medications, check whether any of them are among the drugs with newly negotiated prices. The savings could be significant. You can review the full list at Medicare.gov.

IRMAA Bracket Changes for 2026

If you have higher income in retirement, you are likely familiar with IRMAA, the Income-Related Monthly Adjustment Amount. It is essentially a surcharge on top of your standard Part B and Part D premiums, and it catches many pre-retirees by surprise.

For 2026, the IRMAA brackets increased by approximately three percent, while the surcharges themselves rose by about nine percent. Here is the updated breakdown for single filers:

| Modified Adjusted Gross Income (Single) | Part B Monthly Premium | Part D Monthly Surcharge |

|---|---|---|

| $109,000 or less | $202.90 | $0.00 |

| $109,001 – $137,000 | $284.10 | $14.50 |

| $137,001 – $171,000 | $405.60 | $37.40 |

| $171,001 – $205,000 | $527.10 | $60.30 |

| $205,001 – $500,000 | $648.60 | $83.20 |

| Above $500,000 | $689.90 | $91.00 |

For married couples filing jointly, double each income threshold (for example, the first bracket starts at $218,000).

The two-year lookback rule is critical. Your 2026 IRMAA is based on your 2024 tax return. That means if you had a high-income year in 2024, perhaps from selling a home, exercising stock options, or taking a large Roth conversion, you could be paying significantly higher Medicare premiums right now.

If your income has dropped since 2024 due to retirement or another life-changing event, you may be able to request a reduction by filing Form SSA-44 with Social Security.

Thomas’s Take: IRMAA planning is one of the most overlooked aspects of retirement income strategy. A single Roth conversion that pushes you into the next bracket could cost you thousands in additional Medicare premiums over the following two years. This is why coordinating your tax strategy with your Medicare costs is so important, especially in those bridge years between retirement and age 65.

Free Download: Social Security Optimization Guide

Learn the strategies that could maximize your lifetime Social Security benefits.

Get Your Free Copy

Medicare Advantage: What Is Changing

Medicare Advantage plans, the private-plan alternative to Original Medicare, are seeing several regulatory changes in 2026 that could affect your coverage experience.

Prior authorization restrictions. CMS finalized new rules that restrict Medicare Advantage plans’ ability to reopen and deny previously approved hospital admissions after the fact, except in cases of obvious error or fraud. This is a meaningful consumer protection for anyone who has experienced the frustration of a retroactive coverage denial.

Faster prior authorization decisions. Beginning in 2026, plans must respond to urgent prior authorization requests within 72 hours and standard requests within seven calendar days.

Electronic prior authorization. Plans are required to implement electronic prior authorization systems, which may reduce delays and paperwork for both providers and patients.

Industry movement. Several major insurers, including Humana, have committed to reducing prior authorization requirements for outpatient services in 2026.

If you are currently on a Medicare Advantage plan or considering one for retirement, review your plan’s 2026 Evidence of Coverage document carefully. Network changes, formulary updates, and benefit modifications happen annually.

What This Means If You Are Retiring in 2026

If retirement is on your near-term horizon, these Medicare changes affect your planning in several specific ways:

Your healthcare budget needs updating. Between premium increases and potential IRMAA surcharges, a married couple could pay anywhere from $5,436 to over $18,700 annually in Medicare premiums alone in 2026, depending on income. Build these numbers into your retirement income projections.

Your Roth conversion strategy matters more than ever. If you are considering Roth conversions in the years before or after retirement, model the IRMAA impact. And with the 2026 tax bracket changes adding pressure from another direction, coordinating both together is essential. A conversion that saves you taxes long-term could temporarily increase your Medicare costs. That does not mean you should avoid conversions, but you should factor in the full picture.

Your Social Security claiming decision intersects with Medicare. If you are claiming Social Security benefits, your Part B premium is typically deducted directly from your benefit check. Higher premiums reduce your net Social Security income. This is especially relevant when coordinating spousal benefits with Medicare enrollment timing.

The Part D cap is a real benefit. If you or your spouse takes expensive medications, the $2,100 annual cap provides meaningful protection that did not exist before 2025. Make sure you are enrolled in a Part D plan or a Medicare Advantage plan with drug coverage to take advantage of it.

Three Steps to Take Now

- Review your 2024 tax return for IRMAA exposure. Your 2024 Modified Adjusted Gross Income determines your 2026 Medicare premiums. If you had an unusually high income year and your situation has since changed, consider filing Form SSA-44 to request a reduction.

- Compare your current Medicare plan during Open Enrollment. Whether you are on Original Medicare with a Medigap supplement or a Medicare Advantage plan, evaluate whether your current coverage still makes financial sense given the 2026 cost changes. The Medicare Plan Finder at Medicare.gov is a helpful starting point.

- Coordinate Medicare costs with your broader retirement income plan. Medicare premiums, IRMAA surcharges, Roth conversion strategies, and Social Security timing are all interconnected. Consider working with a fiduciary advisor who can model these variables together rather than addressing them in isolation.

Key Takeaways

- Part B premiums rose to $202.90/month in 2026, an increase of $17.90 from 2025, adding roughly $215 per person annually.

- The Part D out-of-pocket cap is now $2,100, providing a meaningful ceiling on prescription drug costs for all Medicare beneficiaries.

- IRMAA surcharges increased by about nine percent, and they are based on your 2024 income. A high-income year two years ago could be costing you thousands in extra premiums today.

- Medicare Advantage prior authorization rules tightened, with new consumer protections against retroactive denials and faster decision timelines.

FAQ

How much is Medicare Part B per month in 2026? The standard Medicare Part B premium is $202.90 per month in 2026. However, if your Modified Adjusted Gross Income exceeds $109,000 (single) or $218,000 (married filing jointly), you may pay more due to IRMAA surcharges.

What is the Medicare Part D out-of-pocket maximum for 2026? The annual out-of-pocket cap for Medicare Part D is $2,100 in 2026. Once you reach this amount in covered drug costs, you pay nothing for the rest of the calendar year. This cap was established by the Inflation Reduction Act and first took effect in 2025 at $2,000.

Can I reduce my IRMAA if my income has dropped? Yes. If you have experienced a life-changing event such as retirement, reduction in work hours, or loss of income, you may request that Social Security use a more recent tax year to calculate your IRMAA. File Form SSA-44 with your local Social Security office to make this request.

Medicare planning is one of those areas where the details genuinely matter to your bottom line. Even small premium changes, compounded over a 20- or 30-year retirement, can add up to tens of thousands of dollars. If you have questions about how these 2026 changes affect your specific retirement plan, I am always here to help.

Thomas Clark is a Senior Lead Wealth Advisor at Confluence Capital Management, LLC. Investment advisory services offered through Altitude Capital Management, LLC, an SEC-registered investment advisor. Content on this site is for educational and informational purposes only and does not constitute personalized investment advice. Past performance is not indicative of future results. Consult with a qualified financial professional before making any investment decisions.

Thomas Clark is a Series 65 licensed investment advisor and experienced trader. He specializes in investing, retirement planning, and market analysis, helping individuals build wealth and make informed financial decisions.