One of the cruelest surprises in widow’s tax trap retirement planning: after losing a spouse, your taxes can nearly double — even though your income barely changes.

I have seen this happen to clients more times than I can count. A couple files their taxes jointly for decades, paying a reasonable rate on a comfortable retirement income. Then one spouse passes away. The surviving partner’s income drops slightly — maybe one Social Security check disappears — but the tax bill jumps by thousands of dollars. It feels like a punishment at the worst possible time.

This is the widow’s tax trap, and it catches most people completely off guard. The good news is that couples who understand how it works can take steps now to soften the blow. In this article, I will walk through exactly what happens when a filing status changes, show you the real dollar impact through a hypothetical case study, and lay out five strategies that may help reduce the damage.

Table of Contents

- What Is the Widow’s Tax Trap?

- Hypothetical Case Study: Margaret’s Story

- The Social Security Survivor Benefit Wrinkle

- RMDs and the Single Filer Problem

- Five Strategies Couples Can Implement Now

- When to Start Planning

- Key Takeaways

- Frequently Asked Questions

What Is the Widow’s Tax Trap?

The widow’s tax trap is the sudden tax increase that happens when a married person becomes a single filer after their spouse passes away.

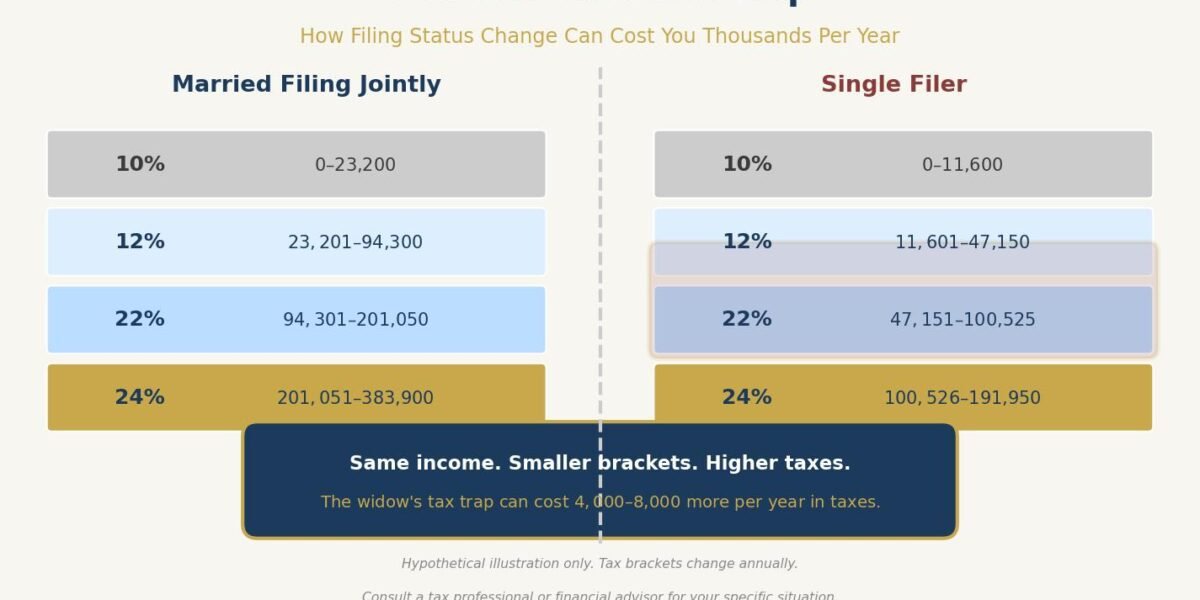

When a married couple files jointly, they get the widest tax brackets the IRS offers. Every bracket threshold — from the 10 percent bracket all the way to the top — is roughly double the threshold for a single filer. That means a married couple can earn significantly more income before hitting the next bracket.

When one spouse dies, the surviving partner may file jointly for the year of death, but the following year they must file as a single taxpayer. The income often does not change dramatically — retirement account withdrawals stay roughly the same, pensions may continue, and the surviving spouse keeps the higher of the two Social Security checks. But the brackets compress significantly.

Here is what the bracket compression looks like for 2026, assuming the Tax Cuts and Jobs Act provisions expire as scheduled:

| Taxable Income | Married Filing Jointly Rate | Single Filer Rate |

|---|---|---|

| Up to $23,850 (MFJ) / $11,925 (Single) | 10% | 10% |

| $23,851 – $96,950 (MFJ) / $11,926 – $48,475 (Single) | 12% → 15% | 12% → 15% |

| $96,951 – $206,700 (MFJ) / $48,476 – $103,350 (Single) | 25% | 25% |

| $206,701 – $394,600 (MFJ) / $103,351 – $197,300 (Single) | 28% | 28% |

Note: Bracket thresholds are approximate for illustrative purposes. If the TCJA sunsets in 2026, pre-2018 rates and brackets return. Consult a tax professional for current rates.

The result: income that fell comfortably in the 12 or 15 percent bracket for a married couple could land in the 25 or 28 percent bracket for a single filer. The same dollars, taxed at a much higher rate.

Hypothetical Case Study: Margaret’s Story

This is a hypothetical example for illustrative purposes only and does not represent any actual client situation.

Profile: Margaret and Richard are both 72. They are retired with the following combined annual income:

- Richard’s Social Security: $2,400/month ($28,800/year)

- Margaret’s Social Security: $1,200/month ($14,400/year)

- Combined RMDs from traditional IRAs: $32,000/year

- Small pension (Richard): $6,000/year

- Total household income: approximately $81,200/year

As married filing jointly, their federal tax bill is approximately $6,200 per year. They are solidly in the 12 percent bracket (or 15 percent if TCJA sunsets), with some income taxed at 10 percent. About 60 percent of their Social Security is taxable based on their provisional income calculation. Life is manageable.

Then Richard passes away.

Margaret’s new income picture:

- Margaret’s Social Security: she drops her own $1,200 check and takes Richard’s $2,400 check as a survivor benefit — $28,800/year

- RMDs from inherited and her own traditional IRA: approximately $30,000/year (slightly lower, but most of the IRA balance remains)

- Richard’s pension: $0 (pension had no survivor benefit)

- Total income: approximately $58,800/year

Margaret’s income dropped by about $22,400. You would expect her taxes to drop proportionally. They do not.

Margaret’s new tax reality:

As a single filer, the bracket thresholds are roughly half of what they were when she filed jointly. Her $58,800 of income — which was comfortably in the lowest brackets as a married couple — now pushes well into the 25 percent bracket as a single filer. Additionally, because the provisional income thresholds for single filers are lower ($25,000 vs. $32,000), up to 85 percent of her Social Security becomes taxable instead of 60 percent.

Margaret’s estimated federal tax bill: approximately $10,400 per year — an increase of roughly $4,200, despite earning $22,400 less than before.

| Married (Both Alive) | Single (After Richard’s Death) | |

|---|---|---|

| Total Income | $81,200 | $58,800 |

| Effective Tax Rate | ~7.6% | ~17.7% |

| Federal Tax | ~$6,200 | ~$10,400 |

| Tax Increase | — | +$4,200/year |

These figures are hypothetical and approximate. Individual tax situations vary based on deductions, credits, state taxes, and other factors. Consult a qualified tax professional for personalized guidance.

That is a 68 percent increase in her federal tax bill on 28 percent less income. And it happens every year for the rest of her life.

Thomas’s Take: The widow’s tax trap is not a rare edge case. It is the default outcome for most retired couples unless they plan around it. The math is working against surviving spouses, and the only way to change it is to act before the loss occurs.

The Social Security Survivor Benefit Wrinkle

When one spouse passes, the surviving spouse does not keep both Social Security checks. They keep the higher of the two and lose the lower one. This is why I emphasize the importance of the higher earner delaying Social Security — that benefit becomes the survivor benefit for the rest of the surviving spouse’s life.

But here is the tax wrinkle: while the household loses one Social Security check (reducing total income), the surviving spouse’s single remaining check may be taxed more heavily because of the lower provisional income thresholds for single filers.

There is also the Medicare IRMAA impact. IRMAA — the Income-Related Monthly Adjustment Amount — adds surcharges to Medicare Part B and Part D premiums for higher-income beneficiaries. The IRMAA thresholds for single filers are roughly half of those for married couples. A surviving spouse who never worried about IRMAA as part of a married couple may suddenly find themselves paying hundreds of dollars more per year in Medicare premiums — on less income.

RMDs and the Single Filer Problem

Required minimum distributions add another layer to the widow’s tax trap. When both spouses are alive, their combined RMDs are spread across the married filing jointly brackets. After one spouse passes, the surviving spouse often inherits the deceased spouse’s IRA — and the combined RMDs from both accounts are now taxed entirely on the single filer schedule.

In Margaret’s case, her combined RMDs stayed close to $30,000 after Richard’s death. As a married couple, that $30,000 sat comfortably in the 12 percent bracket alongside their other income. As a single filer, the same RMD amount pushes her deeper into higher brackets.

Free Download: Social Security Optimization Guide

Learn the strategies that could maximize your lifetime Social Security benefits.

Get Your Free CopyThe problem compounds over time. As the surviving spouse ages, RMDs increase because the IRS life expectancy divisors get smaller each year. More forced income, squeezed into narrower brackets, means the tax bite grows — not shrinks — as the surviving spouse gets older.

Five Strategies Couples Can Implement Now

The widow’s tax trap is not inevitable. Couples who plan ahead may be able to significantly reduce the tax impact on the surviving spouse. Here are five strategies worth exploring with a qualified financial professional.

1. Accelerate Roth Conversions While Both Spouses Are Alive

Roth conversions move money from traditional IRAs to Roth IRAs, paying taxes now at the married filing jointly rates. Once in a Roth, withdrawals are tax-free — and Roth accounts have no RMDs during the owner’s lifetime. Every dollar converted is a dollar the surviving spouse will not have to withdraw from a traditional IRA and pay taxes on at the higher single filer rates.

The ideal window for Roth conversions is often the years between retirement and when Social Security and RMDs begin — when taxable income may be at its lowest. But even after RMDs start, strategic partial conversions can make sense.

2. Review Life Insurance Positioning

Life insurance proceeds are generally income-tax-free to the beneficiary. A properly sized life insurance policy can provide the surviving spouse with tax-free cash to cover expenses during the transition — reducing the need to draw heavily from taxable accounts. This is not about replacing income dollar for dollar; it is about creating breathing room so the surviving spouse can manage withdrawals strategically.

3. Review Account Titling and Beneficiary Designations

How accounts are titled and who is named as beneficiary affects what happens when one spouse passes. Joint accounts, transfer-on-death designations, and beneficiary IRA rules all play a role. Ensuring accounts are structured to give the surviving spouse maximum flexibility — including the option to treat an inherited IRA as their own — can help with tax planning after the loss.

4. Consider a Roth Beneficiary Strategy

If one spouse has significant traditional IRA assets, naming the other spouse as beneficiary (standard) while also building up Roth assets creates optionality. The surviving spouse can then choose which accounts to draw from in any given year, managing their bracket more effectively. Having both taxable and tax-free buckets to draw from is the foundation of the bucket planning approach I use with clients.

5. Accelerate Charitable Giving Using Qualified Charitable Distributions

For couples who give to charity, qualified charitable distributions (QCDs) from IRAs after age 70½ satisfy RMDs without increasing adjusted gross income. This is powerful for any retiree, but especially valuable for a surviving spouse trying to keep income below the thresholds that trigger higher Social Security taxation and IRMAA surcharges. Starting a QCD habit while both spouses are alive builds the strategy into your annual plan.

When to Start Planning

The best time to start planning for the widow’s tax trap is while both spouses are healthy and both incomes are flowing. The strategies above — particularly Roth conversions — work best when you have years to execute them gradually.

Many couples begin this planning in their early to mid-60s, during the gap between retirement and when Social Security and RMDs begin. But even couples already in their 70s can make meaningful progress. Converting a portion of traditional IRA assets each year, reviewing beneficiary designations, and establishing a QCD strategy are steps that can be taken at any age.

The important thing is to not wait until the loss has already occurred. Once a spouse has passed, the surviving partner’s filing status changes immediately and the bracket compression begins. At that point, the planning options narrow significantly.

Thomas’s Take: I bring up the widow’s tax trap in nearly every meeting with married couples. It is an uncomfortable conversation, but the couples who plan for it are the ones whose surviving spouses maintain their standard of living. Ignoring it does not make it go away — it just shifts the burden to the person left behind.

Key Takeaways

-

The widow’s tax trap causes a significant tax increase for surviving spouses — often $4,000 to $8,000 or more per year — because single filer tax brackets are roughly half as wide as married filing jointly brackets, even though income may barely change.

-

Social Security survivor benefits and RMDs compound the problem. The surviving spouse loses one Social Security check but may pay higher taxes on the remaining one, while inherited IRA distributions push income into narrower brackets.

-

Roth conversions are one of the most effective tools for reducing the trap. Every dollar moved to a Roth while both spouses are alive is a dollar that will not be taxed at the higher single filer rates later.

-

Planning must happen while both spouses are alive. Once the filing status changes, the options for mitigation shrink considerably. The earlier couples address this, the more flexibility they have.

Frequently Asked Questions

How long after a spouse’s death does the filing status change?

The surviving spouse may file jointly for the tax year in which the death occurred. Starting the following tax year, they must file as single (or, if they have a qualifying dependent, as qualifying surviving spouse for up to two additional years). The bracket compression hits fully once the single filing status takes effect.

Does the widow’s tax trap affect everyone equally?

The impact varies based on income levels and sources. Couples with higher combined incomes and significant traditional IRA balances tend to feel the largest impact because more of their income gets pushed into higher brackets. Couples with most of their savings in Roth accounts or with lower overall income may experience a smaller shift. Every situation is different, which is why individualized planning with a qualified professional is important.

Can I do anything about the widow’s tax trap after my spouse has already passed?

Yes, though the options are more limited. A surviving spouse can still manage which accounts they draw from, accelerate QCDs to offset RMD income, and consider Roth conversions — though the conversions will be taxed at the higher single filer rates. Working with a financial advisor and tax professional in the year of and immediately following the loss can help identify the best strategies for your specific situation.

Losing a spouse is devastating enough without a surprise tax bill compounding the pain. The widow’s tax trap is one of those quiet risks that most couples never think about — until it is too late to do much about it. But couples who plan ahead can protect the surviving spouse from thousands of dollars in unnecessary taxes, year after year.

If you have questions about how the widow’s tax trap could affect your household, I am always here to help. You can schedule a complimentary consultation to walk through your numbers together.

Thomas Clark is a Senior Lead Wealth Advisor at Confluence Capital Management, LLC. Investment advisory services offered through Altitude Capital Management, LLC, an SEC-registered investment advisor. The information provided is for educational and informational purposes only and does not constitute personalized investment advice. Past performance is not indicative of future results. Consult with a qualified financial professional before making any investment decisions.

Thomas Clark is a Series 65 licensed investment advisor and experienced trader. He specializes in investing, retirement planning, and market analysis, helping individuals build wealth and make informed financial decisions.